This Microcap is making magic out of water and currently prints as an 8x

Metir has mighty upside, but will it make it rain for shareholders?

Welcome back to Wizard’s Winners. Following our deep dive into the subsea cable world of Tekmar, today we are casting our analytical spells over a vastly different, yet equally compelling microcap opportunity.

Meet Metir PLC (LON: MET). At a current share price of just 0.65p (Market Cap ~£2.88m), we are looking at a company at the eye of a high-growth inflection storm. It operates in the decidedly unsexy—but critically essential—world of fast-response water and environmental testing. Metir itself is a derivative of the Latin word ‘to measure’.

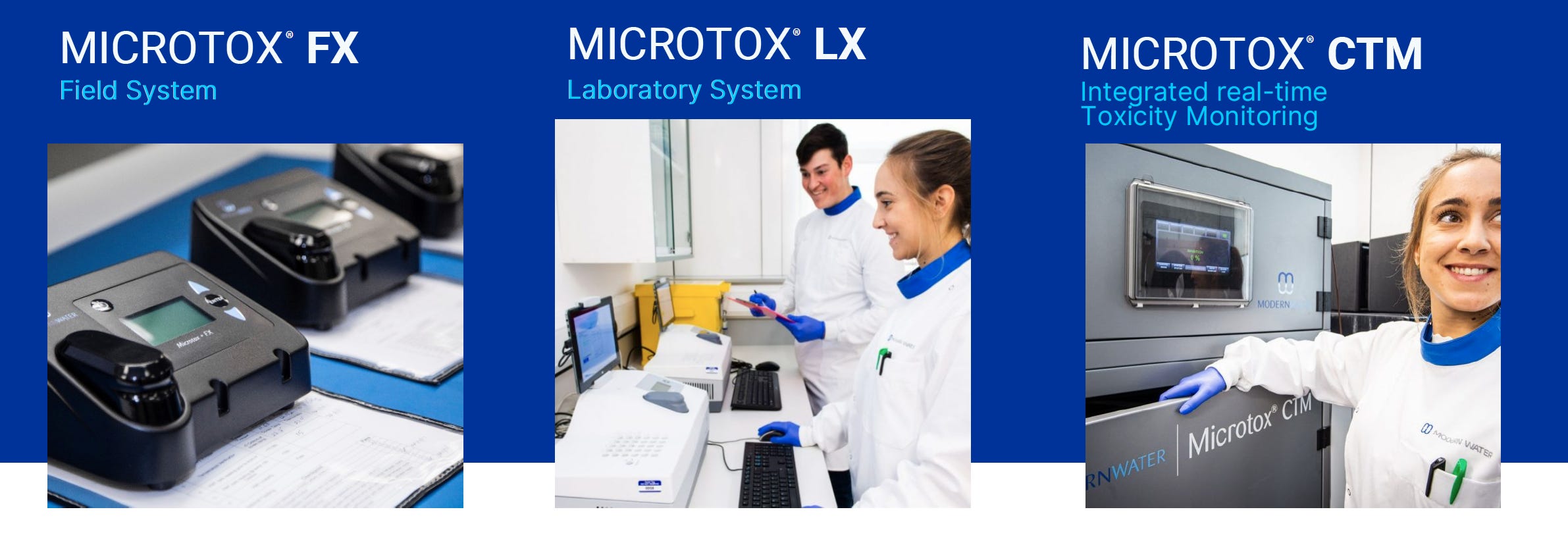

Let’s start with water testing. Traditional lab culture methods for testing drinking water, industrial effluent, and desalination systems take 24 hours to several days to identify toxins. In the world of public health and industrial safety, that delay can be fatal. Metir’s proprietary (and patented) Microtox bioluminescence technology delivers results in minutes. No other company can do this.

Microtox is the established gold standard for rapid toxicity testing (ISO 11348) and has been used at every Olympics since 1984. Needless to say, this alone is a serious intangible moat and probably in itself worth more than the company’s market cap today. One way to think of Microtox is along the lines of this Olympic analogy. Think of it like the Usain Bolt of microbe protection. In this world of The Quick and the Dead, speed really is not only a life or death safety feature, it’s also a vital competitive advantage.

The Business Model Magic: The Razor/Razor-Blade Moat

This is only the start of the opportunity that is Metir. As we will come on to see, for £2m you’re not only getting patented products for rapid testing, you’re also getting a complete testing ecosystem and then some.

While speed is a key advantage, the moneymaking magic lies in Metir’s business model: a classic ‘razor and blades’ approach that as I write is on the verge of a massive operational gearing inflection. This is the Microtox monetisation ecosystem in a nutshell:

The Razor: Metir sells the Microtox LX/FX instruments (the hardware) at a low gross margin (~18%) to penetrate the market, win contracts and secure the install base.

The Blades: Once installed, customers are locked into purchasing the high-margin, recurring reagents required to run the tests. These reagents boast a gross margin exceeding 70%.

This shows us the path towards Free Cash Flow (FCF) inflection: low-margin instrument sales act as a gateway, and once the installed base crosses a critical threshold, marginal revenue drops straight to the bottom line. We are getting closer to this inflection point, though by my analysis we are still probably a year or so away.

That said, sharp-eyed wizards can see that things are already moving beneath the surface. Note these data points for example: Estimated Net Revenue Retention (NRR) is an impressive 125%, with reagent cohorts showing a 15% YoY spend increase. This tells us the company is growing organically and a flywheel effect is forming.

Also, we see the payback period on the Microtox LX/FX instruments is just 8 months. This is supportive of the view that Metir can progress towards that critical FCF inflection point within an annual business cycle.

But these water diviners have more up their sleeves, and it’s even more lucrative…

From Pipelines to Drinking Water

We now look at two further powerful growth drivers the company is seeking to exploit…

Recently, Metir noticed a very big stone in a very big pair of shoes. Time to pay a visit to the microbes eating into the Oil and Gas behemoths.

The microbes bringing down the behemoths:

Pipeline corrosion is a massive, silent drain on the oil and gas industry, costing operators tens of billions of dollars globally every year, with Microbiologically Influenced Corrosion (MIC) accounting for a significant chunk of that.

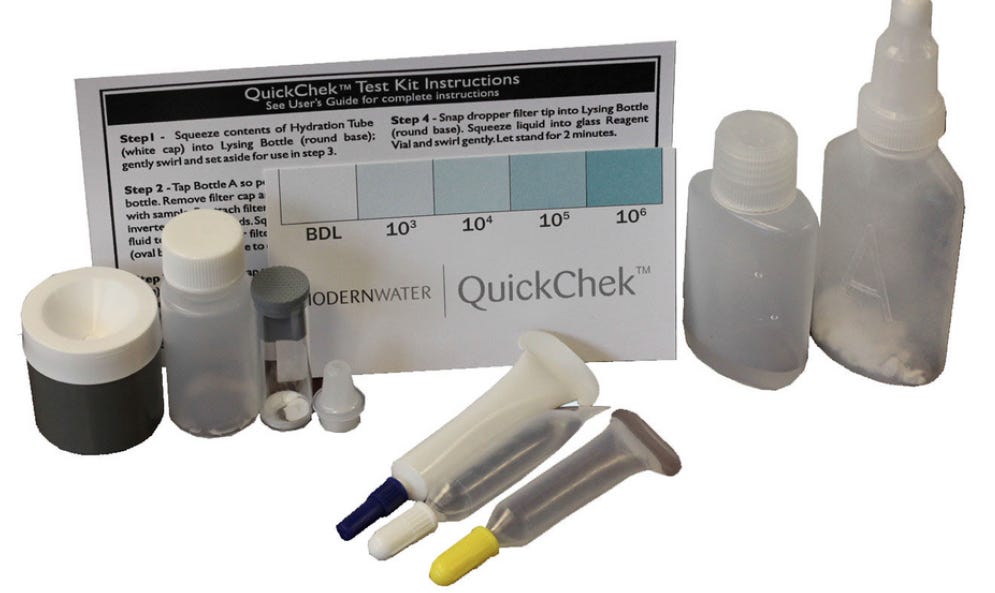

Metir’s QuickChek SRB (Sulfate-Reducing Bacteria) test kit addresses this problem. Used by pipeline operators to detect the bacteria responsible for microbiologically induced corrosion, they are selling these at even higher margins than their standard reagents above. In a June 2025 trading update, management confirmed robust sales and high demand for SRB kits since their launch, with quotations provided to over 60 companies worldwide. Let’s see how many of these quotations are converted into sales at the next results.

So alongside the Microtox and reagents ‘razors and blades’ solution, Metir has another high margin product targeted at the O&G Industry. While competitors like Intertek and ECHA do offer alternatives, Metir’s edge comes from its brand halo, integration with its broader monitoring ecosystem, and first-mover relationships with giants like Aramco.

Municipal Water Blues (Cryptosporidium PD chlorine-resistant pests)

If this isn’t enough, while the core near-term thesis is driven by O&G reagents and SRB kits, Metir is quietly laying the groundwork for a massive expansion into the Municipal/Drinking Water vertical. The upcoming Cryptosporidium PD detector represents significant upside optionality that the market is currently ignoring.

Put simply, in Oil & Gas Services, Metir monitors toxic discharges to protect infrastructure; in Municipal Water, it monitors pathogens to protect public health.

Cryptosporidium is a microscopic parasite resistant to standard chlorine disinfection. Current lab detection takes 24-48 hours—meaning a utility is already in the middle of an outbreak before they know it - lot of good that does then. Metir’s PD detector aims to provide rapid, Usain-Bolt-lightspeed monitoring, changing the paradigm from damage control to prevention.

Take the UK for example. Here water utilities are under immense regulatory and public scrutiny over water quality. No surprise then that pilot testing for the Crypto PD detector has been brought forward to H2 2026, with a potential commercial launch in H1 2027. Crucially, this new ‘razor’ will lock municipal utilities into the exact same high-margin, recurring ‘blade’ (reagent) double act.

How Metir is set up to clean up

So to be clear, Metir currently operates through two subsidiaries:

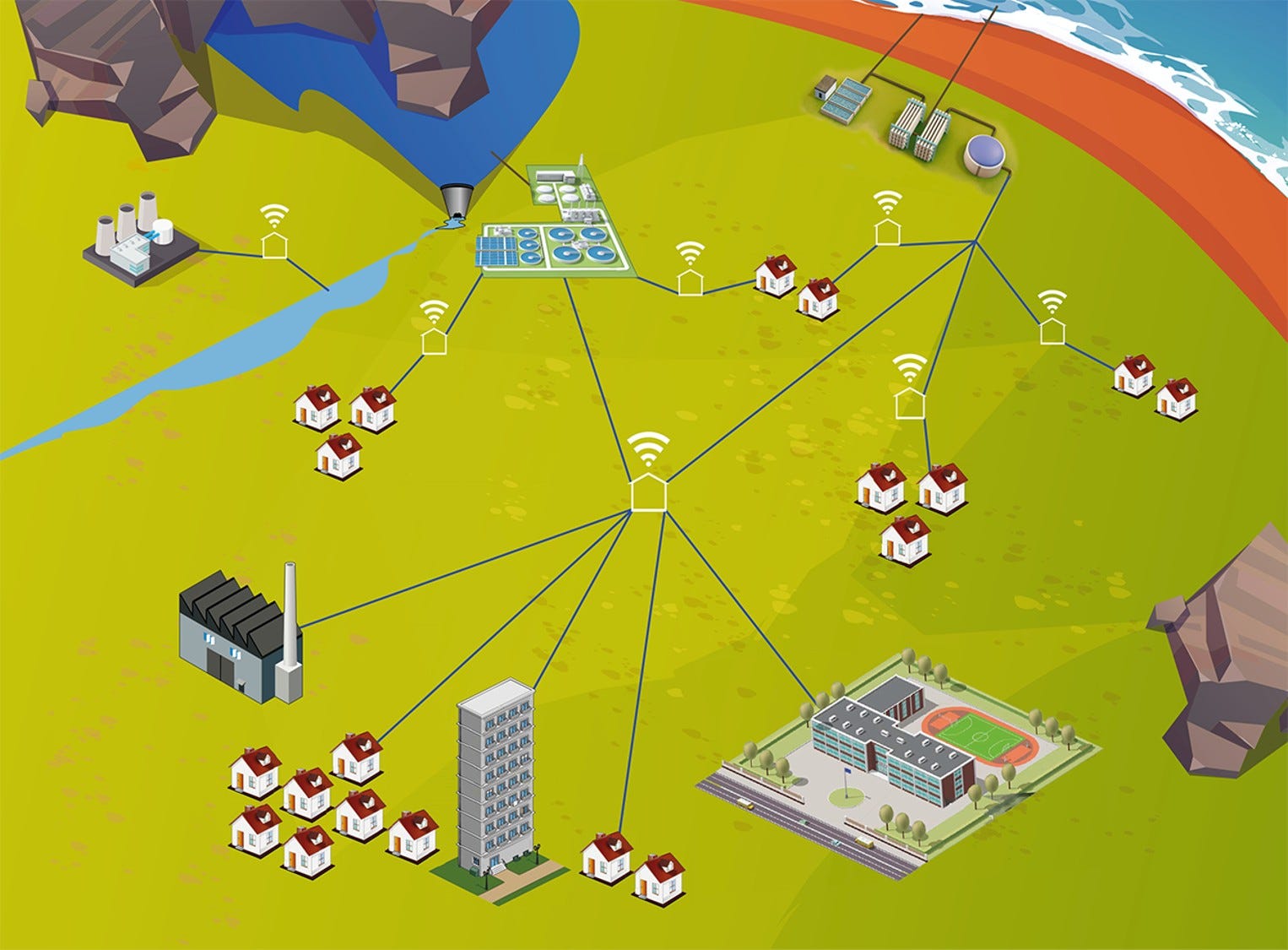

Modern Water focuses on biological and toxicity monitoring. This is the home of the Microtox platform—the gold standard for rapid toxicity testing used to protect infrastructure and public health across diverse sectors, from desalination plants and major global events (like the Olympics) to industrial discharge. They are now layering in high-margin add-ons to this base: pipeline bacteria test kits to specifically combat corrosion in Oil & Gas, and an upcoming parasite detector to expand into municipal drinking water.

Microsaic Systems focuses on chemical detection, specifically tackling the “forever chemicals” (PFAS) crisis with rapid, on-site mass spectrometry for environmental regulators and public water utilities.

The Macro and Market Tailwinds: A Rising Tide

All this jargon and terminology might immediately make you think:

This is a bit niche.

I feel you. So let’s look at the size of the pond Metir is trying to detox.

The Serviceable Addressable Market (SAM) for fast-response/point-of-use water testing is currently £0.8bn, growing at a 10-12% CAGR.

Bearing in mind SpaceX is listing shortly and the CAGR for the go-fast interstellar market is 7% or so, it does demonstrate the old adage that where’s there’s muck, well, there’s brass. No need for rocket science, plain and pure water will do just fine.

Consider the Middle East. In some parts water there is more scarce than on the moon we are told, and thus desalination is quite simply rocketing. That’s Metir’s market.

But then there’s also a determined regulatory push too. Both these factors create a hypersonic tailwind for this lowly UK listed stock. The numbers…

The Desalination Boom: £50bn+ projected capex in the Middle East/Gulf by 2030 under Vision 2030. Metir already has a flagship Continuous Toxicity Monitor (CTM) installation in Qatar (27 units operational).

PFAS & Pathogen Regulation: Tightening global mandates (EU Drinking Water Directive, US EPA PFAS limits, Ofwat Breakthrough Challenge for Cryptosporidium) are forcing utilities to find rapid-testing solutions. Metir’s emerging SRB, PFAS mobile, and Pathogen Detector platforms are perfectly positioned.

Water Stress: Climate change is making water scarcity and quality a global security issue.

The Inflection Point: H1 2025 Surge

In the Wizard’s last post on Tekmar, I highlighted the power of a strategy reboot and how lucrative that can be to shareholders. Hardide (mentioned in the article) has already rocketed over 6x in under 6 months. Tekmar is waiting in the blocks to have its touchpaper lit. Metir by my calculations will be next.

Thus following its 2024 strategic reset, H1 2025 revenue has duly surged 828% to £919k, driven by the Qatar CTM installation and LX instrument sales.

The drop-through maths here is highly lucrative. For every £1m in revenue, Metir sees a 38% gross drop-through to PBT, equating to an EPS impact of 0.11p per £1m revenue. Nice.

Nothing dispels the view that the uptrend can’t continue and Metir’s inflection point is close at hand:

Financial Trajectory:

FY25E: Revenue £1.60m (FCF: -£0.45m)

FY26E: Revenue £3.50m (FCF: £0.20m) Breakeven/EBITDA positive

FY27E: Revenue £5.50m (FCF: £0.60m)

FY28E: Revenue £8.00m (FCF: £1.20m, FCF Margin 15%)

FCF inflection is expected in H2 2027 once installed-base revenue exceeds £2m annually, leveraging the high-margin consumable tailwind. By FY28, the EV/FCF multiple compresses to a mere 2.3x.

Of Dragons and double-edged swords, and Risks and Rewards

Of course, no microcap story is without its dragons and certainly no Wizard worth his salt would ignore them. Metir faces a few.

1. Customer Concentration

The first dragon is that a significant portion of revenue comes from a small group of clients, primarily in the Middle East. The ongoing tensions in the region have already caused friction: a €184k payment from a Qatari customer was delayed in Q1, directly linked to the broader Iran/US/Israel conflict. This highlights the very real short-term working capital risks.

2. The Gulf Conflict as a Double-Edged Sword

At the same time while the war creates short-term payment and logistics headaches, the sustained attacks on vessels and energy infrastructure in the Persian Gulf have led to multiple, well-documented oil spills in 2026, creating a significant environmental crisis.

This pollution directly threatens the seawater intake of the region’s vast network of desalination plants, which must now monitor for toxins more rigorously than ever. Simultaneously, the increased contamination and chaotic operating conditions accelerate the growth of sulfate-reducing bacteria in pipelines, making SRB testing more critical.

So the war is not just a risk; it’s also a long-term demand catalyst. It forces both existing and future customers to consume more reagents and SRB kits to manage the heightened chemical and biological threats. Metir’s products become more rather than less essential in this environment. Thank you to ParThe below for pointing this out.

3. Liquidity and Scale

As a microcap, the stock is thinly traded, and the company must carefully manage its growth capital. The Q1 payment delay is a reminder that even a strong business can face cash crunches. However, the June 2025 fundraise, with its focus on SRB kit capacity, suggests management is steering capital toward the highest-margin, fastest-growing segment of the business.

The latest set of results and Annual Report is due next week. Stay tuned…

The Wizard’s Valuation: DCF & Asymmetry

Ok let’s stack this up. To arrive at fair value, we turn to our Bayesian and DCF models to cut through the noise and find the real picture. Using a 5-year explicit period (2025-2029), a 10% WACC, and a 3.5% terminal growth rate, with a modest 5% accruals haircut for contract timing risk we get these numbers:

Low Case (12% WACC, 2.5% TG, 25% CAGR): £12.1m NPV → 2.73p per share (+320% upside)

Base Case (10% WACC, 3.5% TG, 40% CAGR): £24.7m NPV → 5.57p per share (+757% upside)

High Case (8% WACC, 4.0% TG, 55% CAGR): £37.3m NPV → 8.40p per share (+1192% upside)

So that is an 8x at base case. Can I add anything to that? I don’t know if I can add anything to that.

Catalysts to Watch:

May 2026: FY25 Annual Report (confirmation of reset success).

H2 2026: EBITDA positivity + capacity scale-up.

Q3 2026: Qatar phase-two proposal (17 additional Doha stations) / delayed payments arriving.

FY27: First positive annual FCF.

The Verdict

Metir PLC is a textbook asymmetric microcap bet. It has a proprietary moat (Lightning-fast Microtox IP + 70% margin reagent lock-in), massive macro tailwinds (PFAS, desalination, water security), and a proven razor/razor-blade model reaching operational scale.

However, we must respect that it is navigating something of a narrow strait. The combined Chair/CEO role, historical EBITDA optimism bias, severe capacity constraints, and Middle Eastern geopolitical overtones mean this is still a high-volatility play. Plus, management has single digit % ownership of the company, which is not terrible but we do like to see a bit more skin in the game ideally.

That said, what a business in the making! The strategic vision and capabilities being built look spot on. All for only £2m or so. Dare we say… a drop in what looks like a very large ocean of opportunity.

The upside/downside asymmetry is roughly 8:1.

Target Price Range: 4.5p - 6.0p.

As things stand I am waiting for the Risk/Reward to become more favourable, even if it means sacrificing some upside. Hence I am adding MET to the Wizard’s Winners watchlist.

Let’s wait for capacity scaling confirmation from the GX Group partnership, or a pullback on Qatar payment delays before building a position. The magic is there—but it’s always important to ensure the risk management shield is firmly in place.

Metir PLC MET.L LON:MET #MET.L $MET.L

Extra

Wizard’s Flash Update is here - even more upside!

See the Metir / Turner Pope video interview here (scroll down):

Investors | Metir PLC

Disclaimer: This article is for informational and educational purposes only and does not constitute financial advice. Always conduct your own due diligence.

No 25 accounts out yet. I’ve no idea what cash is like but the auditors will want visibility on a 12 months runway from I assume 30 June 26. Surprisingly heavyweight team of Singers and Turner Pope here. TP have done the historical raises. Last one at 0.75p with 1 for 1 warrants at 2x for 2 years. Better than a heavy discount but a big upside give. That seems to me a repeatable model here. I note Rupert Dyson/Edale capital has a discloseable stake , which is a good sign.

Thanks for the write up on this opaque one. I’ll wait for the raise which looks to be needed for the accounts, but I have a historical position anyhow.

Another important revenue generator not mentioned in your above estimates, with the war forcing SArabia and UAE to make maximum use of pipelines, is and will be (on a bigger scale) sales of SRB kits to oil producers (Aramco is biggest client) and pipeline operators. SRB kits have an even higher - than reagents' - profit margin and it's a near monopoly as this is the market "standard". And, though the war might delay some business, it should also make the use of existing (and future ones) CTMs more critical (thus, bigger consumption of reagents) due to the oil and chemical pollution we are already seeing in the Gulf. So, short term pain but long term gain.