Mkango Mkango, it's time to Tango

Following a frustrating 6 months, Mkango is getting ready to roar again - and it's a 5x from here

A mining company with world class technology set to clean up big time from the West’s rare earths shortage crisis.

Upside: 5x at base case

Risk / Reward asymmetry: 5:1

Mkango is probably an exotic sounding name to international investors. In Malawian it means lion, an endangered species there making something of a comeback in the country.

Equally rare in Malawi are Rare Earth projects with only two currently in advanced stages, one of which is owned by Mkango via its wholly owned Songwe Hill mine. Like the native lion, Mkango is appropriately leading the comeback here too. As many investors know, Rare Earths while being as abundant as nickel in the Earth’s crust are very scarce in the West, with China controlling over 90% of the supply as well as the processing infrastructure.

Mkango is positioned as the comeback king for Rare Earths as whole transforming itself into a one-stop shop for all things Rare Earths. More anon.

Our story begins in Malawi, and from that we’ll see how from this nondescript hill Mkango has become a roaring tech play with quite possibly the hottest technology in world mining.

Before appraising Mkango as an investment, let’s understand the business first. It has three principle business units:

‘Upstream’ - the Songwe Hill Rare Earths mine

‘Midstream’ - Rare Earth separation, based in Mkango’s hub in Poland (Pulawy)

‘Downstream’ - Rare Earth patented ‘short loop’ recyling, enabling rare earth magnets to be recycled from used ‘feed’ like hard drives and ____ at lower cost and greater efficiency than any other process available today.

We can call this a ‘three legged stool’. Each leg has significant value and each leg is arguably by itself worth more than the entire MCAP of Mkango as a whole.

Let’s start our investigation with the first leg, the upstream asset that is the Songwe Hill Mine.

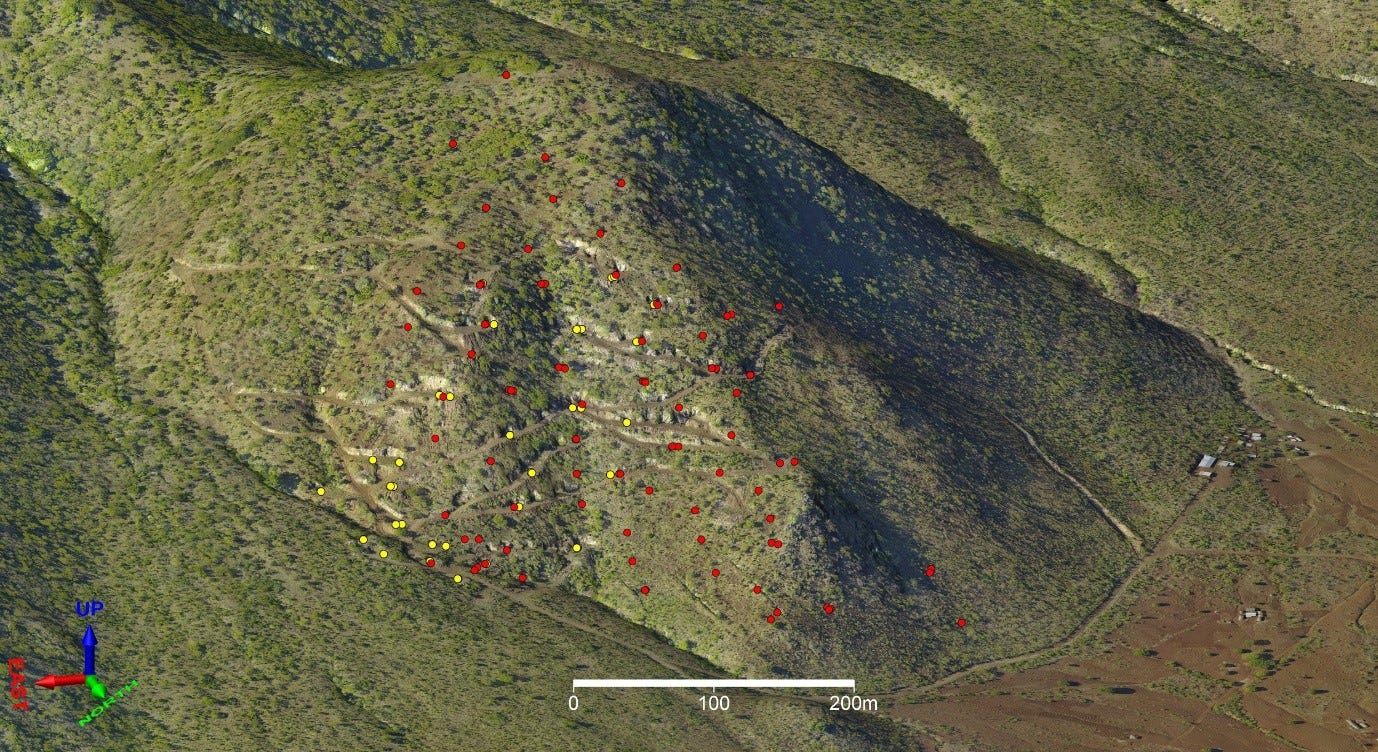

Songwe Hill - Mkango’s rare earth mine (upstream mining)

Songwe Hill contains high concentrations largely of this:

This is neodymium. Neodymium is used in varying quantities for everything from wind turbines, robotics, EV motors, missile systems and defence and aerospace applications. In short, just about every area essential for the so-called new economy.

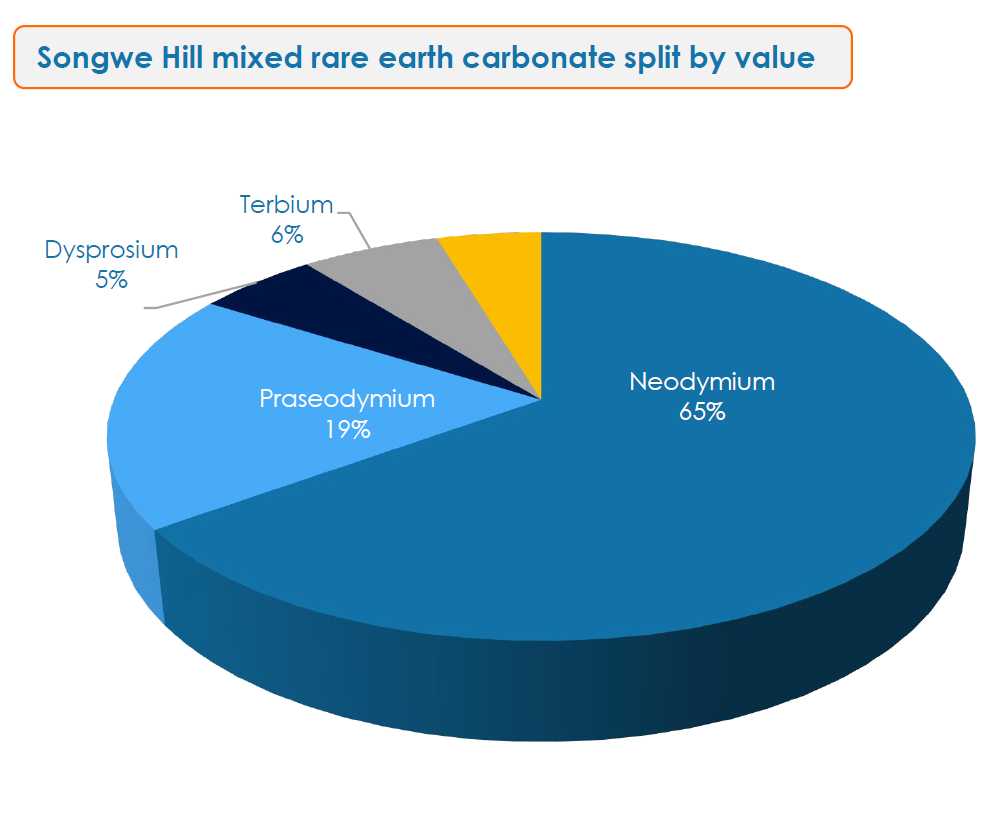

There are other rare earths in Songwe too shown below, as well as thorium (which may replace uranium in nuclear reactors).

Most investors won’t touch mining companies with a perception perhaps of the cyclicality of these kinds of businesses. But let’s bear in mind here with shortages in REEs now becoming extreme, every country is scrambling to secure its supply of the metals. This forms the perfect setup for Mkango shareholders. Let’s look at what’s happened to the neodymium price lately:

It has nearly doubled in a year.

Mkango is very leveraged to the price of neodymium. Each 10% increase in the price of the neodymium adds 21% to the company’s NAV.

Unsurprisingly this has played out in the valuation of Songwe Hill. A recent update to its DFS (Definitive Feasibility Study) clocked the net present value at $339m. Mkango’s MCAP at the time of writing is $278m. So Songwe Hill alone is worth more than Mkango’s mcap as we speak.

Songwe Hill has a projected 18 year mine life and there’s no reason why this might not be extended with further exploration. It also has received EU CRMA Strategic Project status as one of only 13 international projects, further derisking the project. Discussions are also underway for a DFC loan from the US for around $100m which, if confirmed would be another major boon to the project. What we see here is that many of the risks typically associated with mining companies have been removed, given the strategic importance of Songwe Hill.

The Pulawy Rare Earth Separation Plant (midstream refining)

If Songwe Hill is the source, Pulawy is the refinery. This is where the economics get seriously interesting.

Most rare earth miners dig up ore, process it into a mixed concentrate, and then sell that concentrate to… Chinese processors. They capture the low-margin, high-risk end of the business and hand over the most profitable part of the value chain to the very monopoly they are trying to bypass.

Credit to Mkango’s leadership when we see they aren’t playing that game.

Once Songwe Hill is operational, it will produce a Mixed Rare Earth Carbonate (MREC). That MREC will not be sold at a discount. It will be shipped to Poland, to Mkango’s wholly owned separation plant in Pulawy, where it will be broken down into high-purity, individual rare earth oxides. Think of it as turning crude oil into petrol, jet fuel, and plastics. The value uplift is enormous.

The numbers from the March 2026 Pre-Feasibility Study (PFS) are frankly eye-watering but unfortunately the market hasn’t woken up to it yet. Pulawy has a post-tax Net Present Value (NPV) of US779million. Those are world-class project economics by any measure.

Returning to Mkango’s MCAP, Pulawy’s base case NPV is approximately 2.8 times where it’s at today.

Keep score dear acolyte! So Songwe Hill is over 1x MKA’s mcap, now Pulawy is 2.8x more. And we still haven’t got onto the really magical leg of the business yet.

What drives these eye-watering returns? Two things: location and cost.

The site sits on an eight-hectare plot in a Polish Special Economic Zone, adjacent to Grupa Azoty Pulawy’s massive fertiliser and chemicals complex. This is structural genius. By co-locating next to Europe’s second-largest nitrogen fertiliser manufacturer, Pulawy has direct access to the key reagents and utilities required for rare earth separation, including nitric acid and ammonia, via pipeline. This avoids high-cost logistics and the requirement to truck in hazardous chemicals. The PFS puts separation costs at just US$2.14 per kilogram of rare earth oxides, so being at the lowest end of the global cost curve and lower than many Chinese refiners for rare earth separation it really is world class.

Strategic Status and European Backing

But the most compelling angle for investors is the political tailwind. In March 2025, Pulawy was designated a Strategic Project under the European Union’s Critical Raw Materials Act (CRMA). Under the CRMA, the EU assessed the project as being ‘highly important to the EU’s supply security of strategic raw materials’ with ‘viable technical feasibility within reasonable timeframes.’ This is not just a token bureaucratic halo-gesture and carries real value. Strategic status provides a fast-tracked permitting process and access to EU funding support, significantly de-risking the development timeline.

Why would the EU throw its weight behind a Polish plant fed by a Malawian mine? Because Europe is desperate to break China’s near-monopoly on rare earth processing. Pulawy is designed to produce exactly the materials the EU needs: 2,050 tonnes per annum of Neodymium-Praseodymium (NdPr) oxides for EV motors and wind turbines, plus a Heavy Rare Earth Enriched Carbonate (HREC) containing Dysprosium and Terbium for high-temperature and defence applications. It is a direct solution to a critical supply chain vulnerability.

So that is leg number two. A midstream asset with a base case NPV nearly three times the entire company’s market cap, sitting in a friendly jurisdiction with EU strategic backing and world-class cost economics.

Let’s turn to third leg of Mkango’s stool, Hypromag.

HyProMag: The Short‑Loop Recycling Revolution (downstream recycling)

Let’s turn to the third leg of Mkango’s stool: HyProMag.

If Songwe Hill is the source and Pulawy is the refinery, HyProMag is the recycling powerhouse that closes the loop. This is where the company truly separates itself from every other rare earth play on the board.

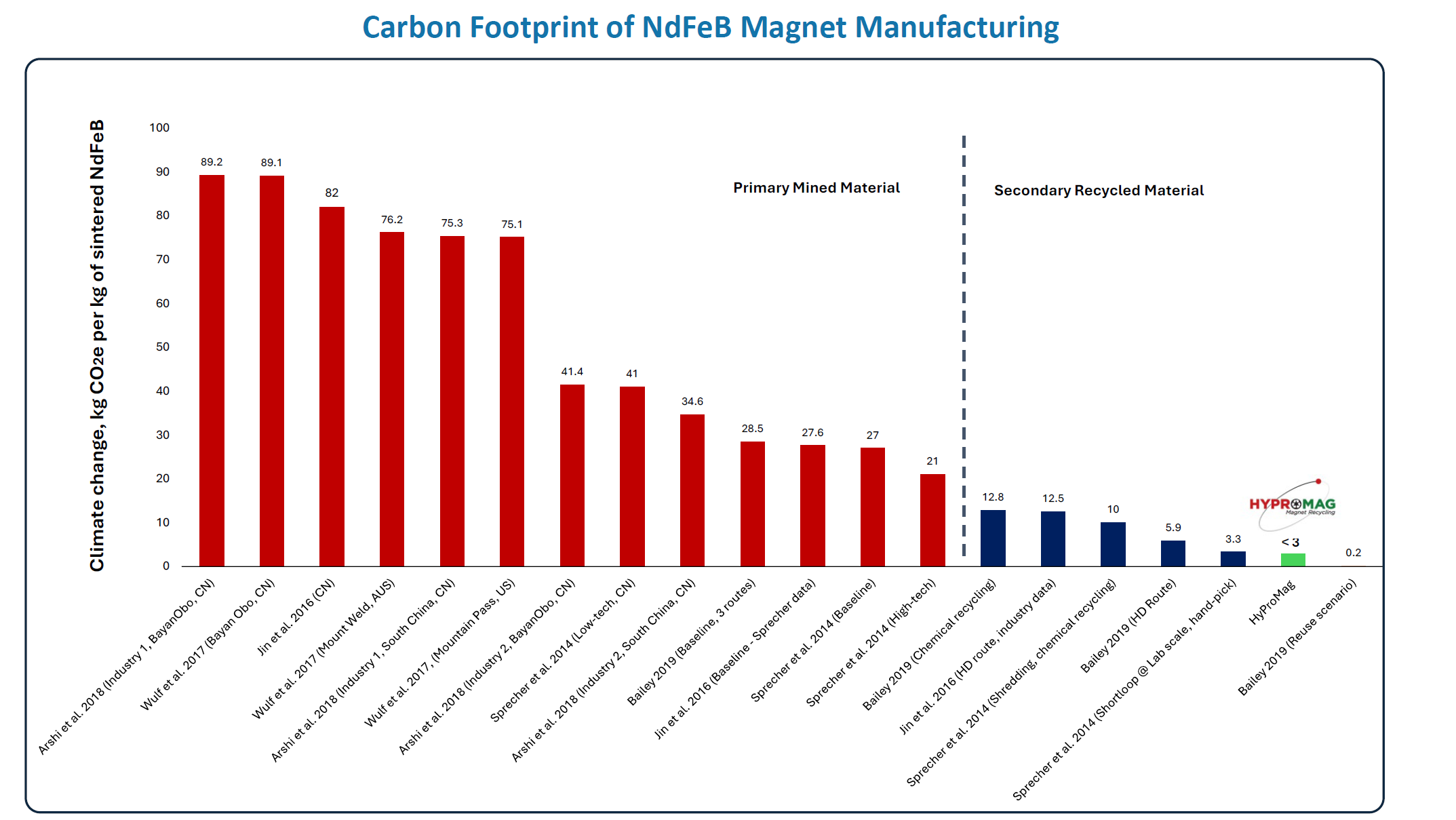

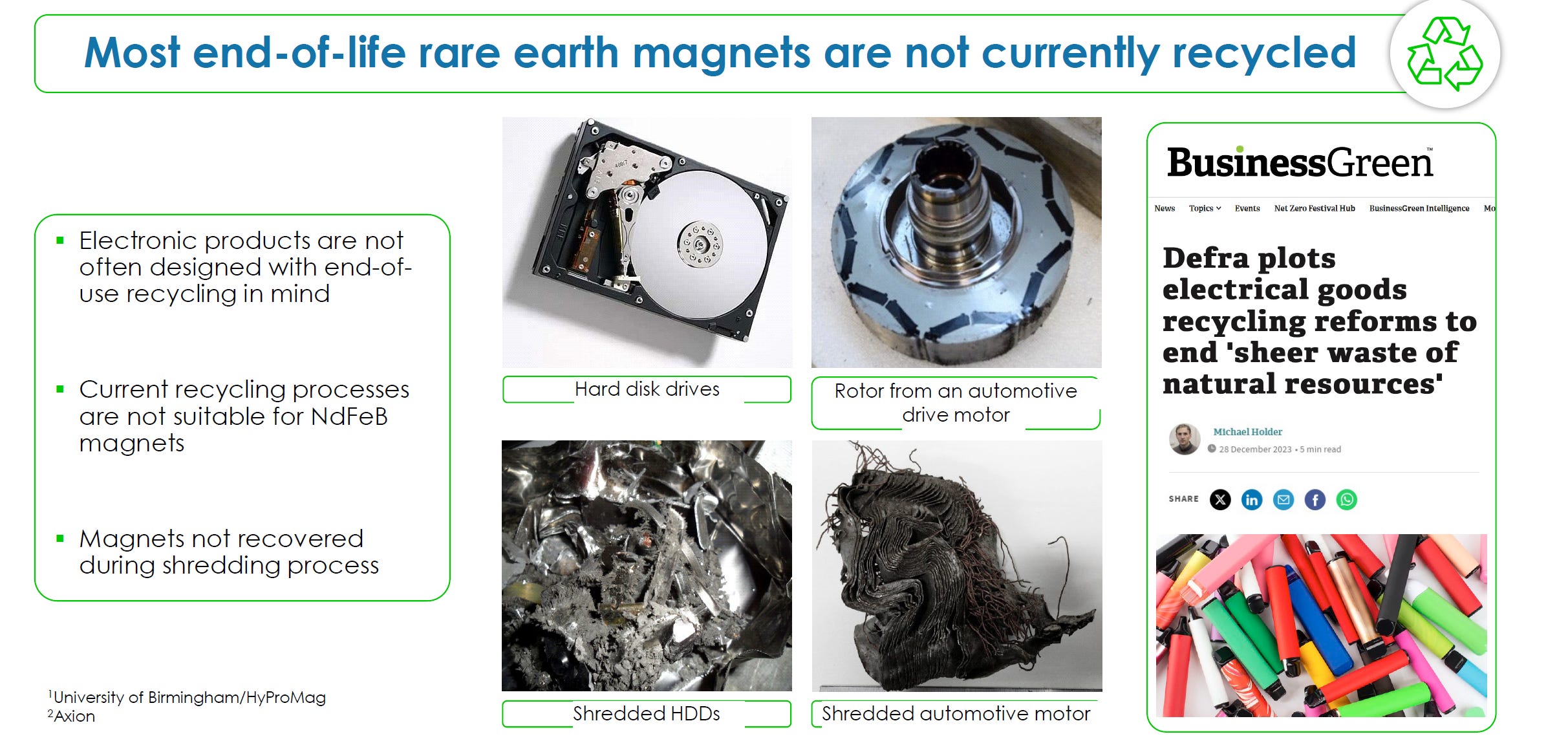

The recycling of rare earth magnets has long been the holy grail of the critical minerals industry. Magnets are embedded deep inside end-of-life products like hard drives, electric vehicle motors, wind turbines, and even e-scooters. Getting them out has traditionally required energy-intensive dismantling, shredding, and chemical vats. The costs quickly pile up. The carbon footprint balloons. And the economics often fail to make sense.

HyProMag has solved this.

Its patented Hydrogen Processing of Magnet Scrap technology, or HPMS, uses hydrogen gas to demagnetise and break down NdFeB magnets inside a sealed vessel. The rare earth powder is then separated from other materials without any chemicals, using just 12% of the energy of conventional methods. Have a look:

This really is world class technology and world class innovation. Credit all those from Birmingham University who painstakingly developed it.

Once separation is complete,. the recovered powder is purified and remanufactured into sintered magnets with 95% recycled content and an 85% lower carbon footprint. It is the only short-loop magnet-to-magnet recycling process in commercial production anywhere in the world.

Short-loop is the key phrase here. Most recycling is long-loop: the magnets are processed back into rare earth oxides, which then have to be re-separated and re-metallised. That is expensive, environmentally unfriendly and time-consuming. Short-loop skips all of that and goes straight from scrap to new magnet. It is faster, cheaper, and greener.

Over US$100 million of R&D has been poured into the technology at the University of Birmingham. HyProMag UK is already in commercial production. As of May 2026, the company has produced 9.2 tonnes of recycled NdFeB alloy powder, of which 7.4 tonnes have been shipped to customers. More than 20 potential buyers have received magnet samples, with customer qualification programmes now accelerating.

The UK facility at Tyseley Energy Park was officially opened by the UK Minister for Industry in January 2026. It has an initial capacity of 100 tonnes per annum on a single shift, expandable to 350 tonnes on multiple shifts. And the company is already evaluating a further expansion to 1,000 tonnes per annum.

Then, on 28 April 2026, Germany went live. The Pforzheim plant was officially opened by the German Federal Ministry for Economic Affairs and Energy. This is not a minor ribbon-cutting. A federal ministry presides over the opening when the technology matters to national security. And it does. The German plant is fully permitted for up to 750 tonnes per annum, with an initial capacity of 100 tonnes ramping up through 2026 and 2027.

The US is next. HyProMag USA is a 50/50 joint venture with CoTec, with CoTec fully funding the development. The Texas hub is targeting 1,552 tonnes per annum of NdFeB magnets and co-products, with first production expected in mid-2027. The US Export-Import Bank has issued a letter of interest for up to US$92 million in financing. Expansion concept studies for South Carolina and Nevada hubs could triple US capacity by 2029. A separate US listing for HyProMag USA is under active consideration for late 2026 or early 2027.

Japan, Canada and South Korea are on the roadmap with discussions currently taking place. Japan we are told has the greatest magnet scrap resource in the world.

Every additional Hypromag plant is worth between $260m to $600m in NPV to Mkango - so its MCAP again for each new one.

But let’s restrict ourselves to the present portfolio and calculate what it’s worth to Mkango.

Hannam’s (the company broker) values the HyProMag recycling portfolio at approximately $923m on a risked and attributable basis - so more than 3 times MKA’s MCAP again.

Let me repeat that: the recycling division alone is worth more than three times the whole company.

So where does that leave us?

Songwe Hill: 1.2x MKA’s market cap.

Pulawy: 2.8x MKA’s market cap.

HyProMag: 3.3x MKA’s market cap.

Add them up and you get a sum-of-the-parts value of approximately 7.3 times the current share price, before any risk adjustment. Even after applying conservative execution discounts, the base case valuation still gives us a 5x upside.

Three world-class businesses, each one arguably worth more than the entire company by itself, packaged into a single London- and Toronto-listed entity trading at 51p.

Myles McNulty compared Mkango with its listed peers on his X account. The valuation disconnect is extreme:

Given that in its current trajectory Mkango is due to produce the same amount of NdPr as MP Materials Corp plus has superior technology, why is it trading on a multiple that is a whopping 42x lower?

C’mon give me a break.

Let’s look at Cashflows

Admittedly this is still academic unless the company can generate the FCFs to realise the value we can now clearly see. The market seems to doubt it can, or (more likely) doesn’t understand the opportunity and has summarily dumped it into the too difficult bucket.

Fair enough. Development‑stage resource companies burn cash. Construction costs are lumpy. Permits take time. And Mkango has five simultaneous assets in various stages of development. Quite a few spinning plates there for sure.

But here is where the market is wrong.

The company has not one but two engines already generating revenue. HyProMag UK produced 9.2 tonnes of recycled NdFeB alloy powder in 2025 and shipped 7.4 tonnes to customers. HyProMag Germany meanwhile is now up and running. So ever so quietly Mkango is already cash generative.

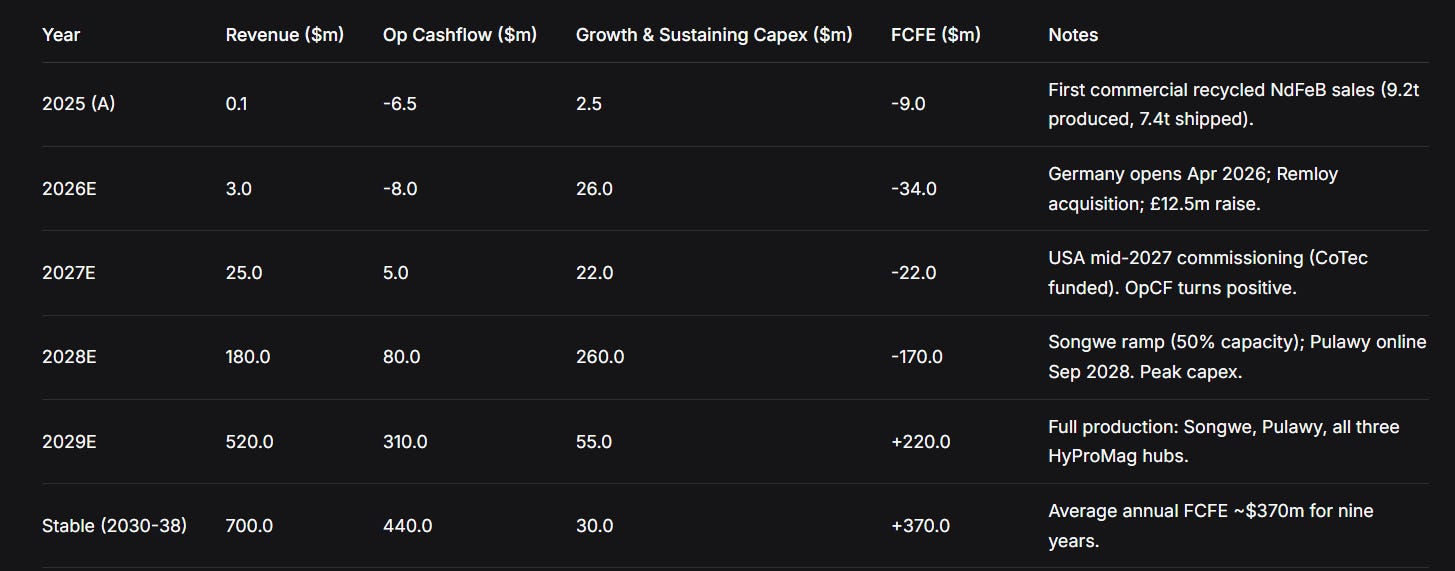

The table below lays out the cashflow trajectory year by year, based on the company’s feasibility studies, Hannam’s modelling, and a conservative US110/kg NdPr price, below current spot, and the Wizard’s own causal and dynamic factors.

Let’s break down how Mkango is finding its roar over time:

2025-2026: Classic development burn. Cash outflow peaks at US$34m in 2026. This is the phase the market sees and fears.

2027: Operating cashflow turns positive for the first time (US$5m) as HyProMag USA comes online (CoTec funded). FCFE still negative, but direction is clear.

2028: Peak capex year. Songwe ramps to 50%, Pulawy commissions. Revenue jumps to US180m, operating cashflow to $80m, but growth capex hits US260m. NetFCFE−$170m. This is the gap the SPAC (where Songwe Hill is listed on NASDAQ) and DFC grant bridge. So there is no cause for alarm here.

2029: The inflection point. Full production across all assets. Revenue hits $520m, operating cashflow $310m, FCFE turns positive at US$220m.

2030-2038: Stable state. Annual FCFE averages US$370m over nine years.

Now put those numbers in perspective.

$370m of annual FCF at a 10x multiple is $3.7bn — more than 13 times today’s EV of US$275m. Even after risk discounts, the base case 5x return from 54p stands.

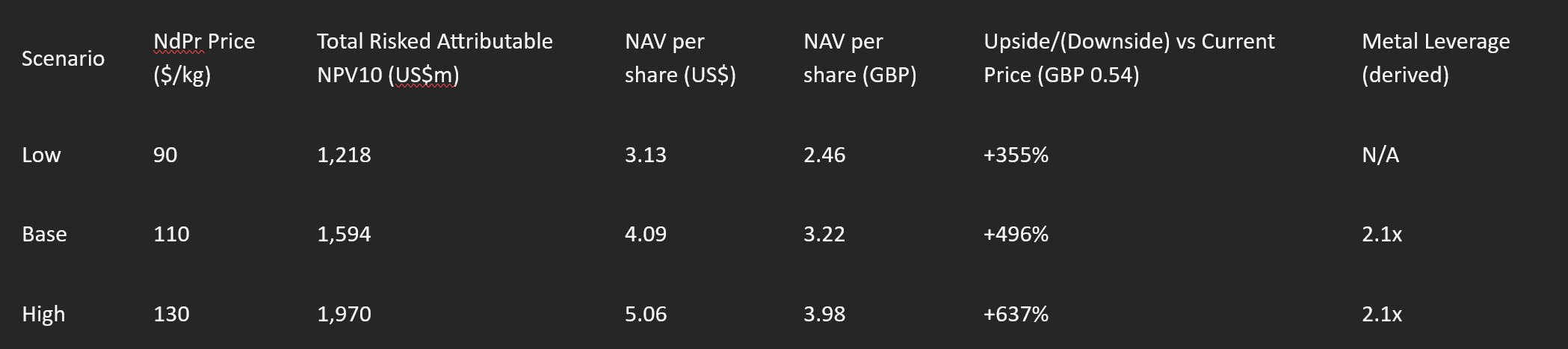

Meanwhile my own DCF derived NPVs come to this:

So a comfortable 5-6x at base case. And for every additional Hypromag plant licensed, you can add another x.

The market sees a cash-burning junior. The numbers show a cash-printing machine waiting to be switched on. Three world-class businesses, each worth more than the whole company, packaged into one London-listed stock at 54p. This is the setup. That is the thesis.

So yes, Mkango Mkango, it really is time to Tango.

Disclosure: This is not financial advice. The author may hold positions in the mentioned securities. Always do your own research.

Thanks for the article!

A few remarks only. Songwe Hill project also got EU CRMA designation last spring as one of 13 projects geographically out of Europe. Thus Mkango is the only I heard about to have two EU CRMA designation in paralel. Also: DFC loan around 100m usd is under consideration for the Songwe Hill project. (Showing interest and backing from the US and EU at the same time. Direct and indirect stakes on HyProMag US is around 60/40 % for Cotec and MKA.

I really missed elaborating the MKAR spac merge Nasdaq listing story, which may be a huge value driver in the near future.

And a few words about the personal and institutional interconnections within this industry (from Cohen &Co (dealt with other listings such as USAR,CRML, EMAT, to Mr. Manadou (ETM, EMAT etc).

But I think your piece is a useful read for anyone to get familiar with this excelent opportunity