James Cropper Flash Update - Stirling effort!

The Wizard is buying more of tomorrow’s Filtronic

‘Sometimes the old ways are the best ways’

James Bond, Casino Royale.

James Cropper CRPR.L #CRPR.L 378p

Following on from the Wizard’s Filtronic post yesterday, we go from one end of the aerospace stock universe to the other.

From a massively overpriced Elon Musk associated whizzbang stock market darling to a small, unknown, unloved paper company with a dated factory in the Lake District UK - in short a company as far away from the space meme theme as you might expect.

Today James Cropper dropped a hugely important RNS.

Our thesis is playing out

Today’s RNS has seen the company replace its existing setup with a new, flexible £15m invoice discounting facility committed for at least three years. Part of this move sees them paying off £7.1m of their current UK bank loan using cash on hand, pushing the remaining balance out to 2030, and extending their US bank loan maturity.

At the same time they have smoothed out their pension scheme schedule, dropping near-term contribution requirements.

The significance of this is this completely removes the balance sheet stress the market seemed to be fixating over. Any lingering fears of a near-term cash squeeze are now officially dead.

This is what we wrote on our May 27 Wizard’s Winners analysis:

The Balance Sheet shows the investment journey clearly progressing from ‘fusty industrial’ to ‘compounding machine’.

That has now happened, you can read it in the RNS. Great job guys!

Summary of the Refi:

Cleared off expensive debt: James Cropper are using cash on hand to pay off £7.1m of the old loan immediately. This immediately lowers their ongoing borrowing costs, leaving more free cash inside the business.

Pension drain plugged: While they made a one-off £0.6m payment into the pension scheme, they successfully negotiated a £0.35m reduction in required contributions through September 2027, freeing up liquidity right now.

James Cropper is woefully misunderstood - and mispriced

James Cropper is significantly mispriced at 380p. Total net debt now sits comfortably at less than 1x earnings, yet. The market continues to price this as a heavily indebted old-school paper mil, but this move proves the financial foundation is rock solid while we wait for the high-margin aerospace and defence turnaround to scale up.

The James Cropper thesis we wrote about originally rested on

Balance sheet deleveraging (job done - today’s RNS),

Pivoting more towards the ‘sexy’ Advanced Materials side. This is the high margin and high CAGR hydrogen, aerospace, batteries and wind energy division. Currently 35% of the business, we are looking for this to increase

Further Contract wins

A brand move from a ‘paper’ company into an AEROSPACE AND DEFENCE company.

Maintaining and growing its exceptional technical and technological moats

In today’s update we want to focus on the central catalyst of this story, and it is being majorly underappreciated.

The new CEO is a seriously heavy hitter - and he means business

James Cropper’s new CEO (David Stirling) joined the company last year. This is, if I may say, a serious coup by the company.

Prior to joining James Cropper, he was the CEO of Zotefoams plc for 24 years. That’s right, he’s the guy who built Zotefoams into what it is.

He built Zotefoams up from a single site in the UK to establishing multiple manufacturing operations across the UK, Europe, North America, and Asia, successfully developing a range of technical materials to serve a diverse, global customer base. In short, from a fusty old factory into an absolute world class business serving the likes of Nike, Boeing, Airbus and Technifab. See the aerospace connection with James Cropper?

We think this should count for something, even if the market doesn’t. Maybe the market is asleep? Or still swooning over trips to Mars?

Now let’s look and see what Mr Stirling has done in the short time he has been here. The list is long so I’m cutting it down to the purely financial and commercial details:

Financial Turnaround & Earnings Outperformance

EBITDA and Profit Beat: Under his execution of the June 2025 strategy, the Group’s FY26 Adjusted EBITDA is expected to land at £8.8m - approximately 10% ahead of market expectations and a massive 31% increase year-on-year.

P&P Segment Stabilization: He successfully turned the historically loss-making Paper & Packaging division EBITDA-positive in the second half of FY26 through strict operational cost efficiencies, keeping the business on track to hit its run-rate break-even target.

Advanced Materials Momentum: Advanced Materials delivered low double-digit revenue growth in FY26, keeping the group’s long-term high-margin growth engine well-funded and structurally sound.

Commercial Realignment & Operational Discipline

The ‘3 Peaks’ Manufacturing Pivot: Stirling completely re-engineered the Paper & Packaging business model after identifying functional disconnects in legacy management. He re-introduced commodity filler grades (Peak 1) to stabilize machine utilization, correcting a flawed prior strategy that left assets severely underutilised (this has cashflow impacts, see anon)

Resilient Merchant Backfilling: When a major coloured paper merchant exited on short notice in July 2025, Stirling’s team swiftly backfilled the utilization void with alternative direct brand relationships and swing volumes, leaving FY26 P&P revenues flat year-on-year despite the customer loss. This is actually brilliant!

Strategic Growth Alliances: He capitalised on technical capabilities by launching Ready2Stack™ in collaboration with HOERBIGER to target the hydrogen economy and spearheaded a high-value carbon recycling partnership with Hexcel in March 2026.

Non-Core Asset Monetisation: In May 2025, he optimized the portfolio by disposing of non-core intellectual property rights, generating an initial €1.75m in cash while retaining fee-free operational licenses for internal use.

A Stirling effort, if I may say - and he’s only been in the job a year or so! Can you see where this is going though?

A Note about the Factory

In yesterday’s post we covered a company (Filtronic) which has invested heavily into a brand new state of the art facility.

James Cropper has an old very dated factory. The downside of this is pretty obvious, it is not cost efficient and does lead to high operational gearing. But let’s look at the upsides and see if there really is something to James Bond’s sometimes the old ways are the best ways epithet:

No nosebleed capex

Unmatched Customisation: The multi-purpose machines can run a wide range of complex specifications and highly specific coloured papers that competitors simply cannot replicate on a global scale.

Agile Production Runs: The factory has the unique ability to seamlessly switch between very small, bespoke luxury production runs and large-scale industrial campaigns using the exact same assets.

Product Differentiation: The combination of older, adaptable machines and deep technical expertise allows the company to innovate and develop highly differentiated, premium materials.

Give me a choice between the two - Filtronic’s highly specialised brand new shiny scimitar and James Cropper’s seemingly crappy old Swiss Army knife which nonetheless can get any job done albeit less efficiently yet in an agile way allowing it to avoid working capital crunches - and for me it will be the Swiss Army knife seven days a week and twice on Sundays.

Your CEO has previously touched on this dilemma and knows what he is doing in my view, let’s give him the benefit of the doubt.

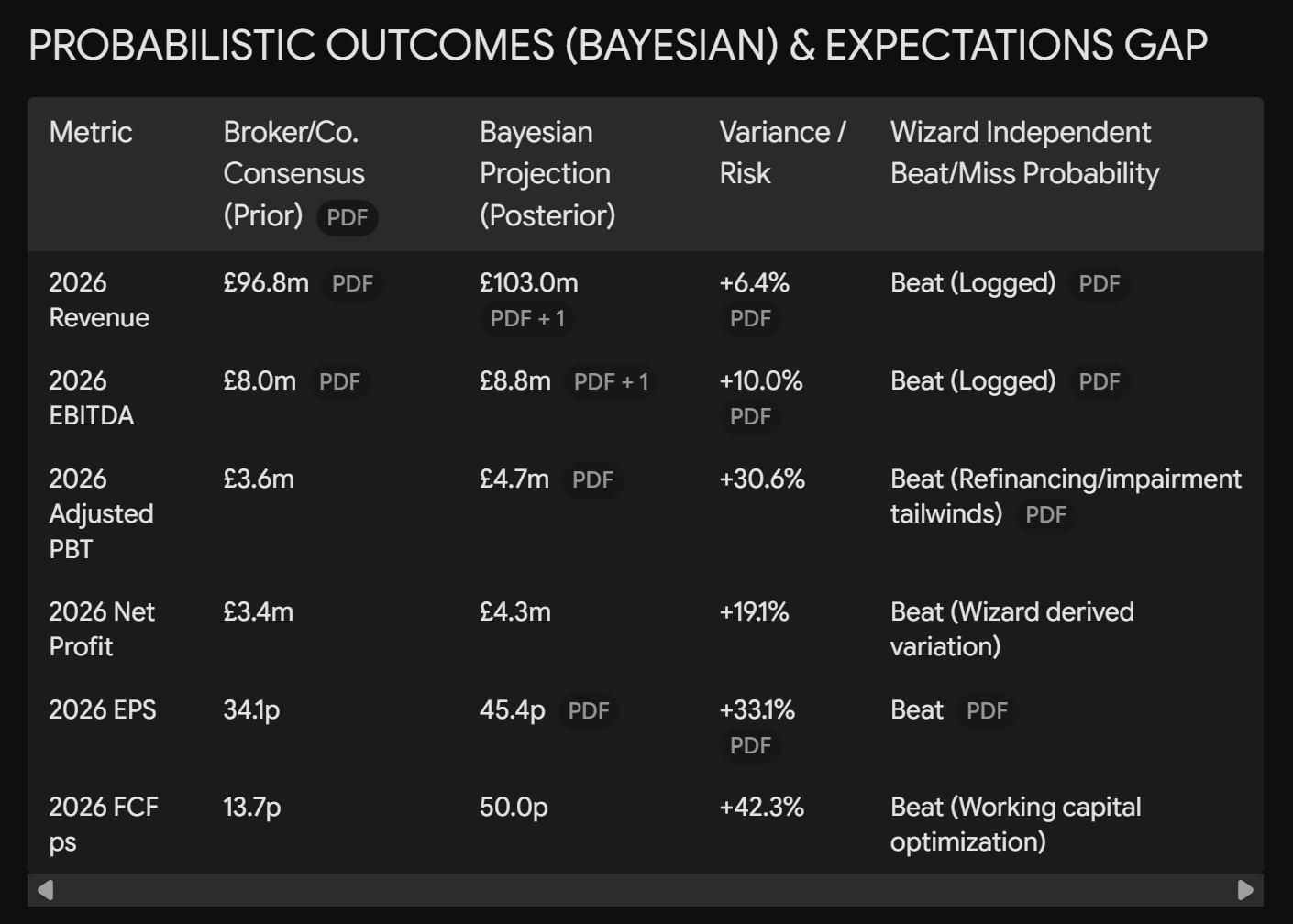

Final Results on 21 July - what is Wizard predicting?

Wizard (our predictive engine) is currently forecasting FY numbers in line with management and broker forecasts, but with a significant beat on Free Cashflows (ok no one cares about those, but we do - a lot. Also this is in a large part due to the CEO’s financial and operational strategy).

However, today Wizard issued an NLP (Natural Language Processing) flag after analysing the language in the RNS.

The language is very optimistic, it tells me. I check previous NLP analyses and see management has a history of conservativism - this then is a flag to pay attention to.

Unfortunately due to a lack of primary source information, we cannot update our predictive priors but if we were gambling men here, we’re feeling an increased probability of a BEAT on top-line numbers. So predictions are i) a definite beat on FCF forecasts and ii) a gambling man’s beat (ie higher probability than 50%) on all numbers.

Here’s what we’re going with. The Broker/Company guidance is in the second column, our predicted numbers in the third:

As a note to this, we can’t reconstruct the company’s source numbers (confidentiality constraints) so this is going to be lower in accuracy. But we are going for across the board beats. And I am going to really stick my neck out here and say that Cropper’s FY results will even beat Wizard’s own projections.

The Wizard continues to add.