Cindrigo... should I go?

A European Geothermal opportunity trading at less than a tenth of its listed peers offering potentially SEISMIC returns

Upside: 10.3x at base case

Risk / Reward asymmetry: 17.2 : 1

Cindrigo Holdings plc CINH.L 4.75p £15.8m / $21.1m MCAP

A 10x upside, really? Oh what, might that be a 23x upside? Achtung Baby!

Today we cast our curious gaze over a geothermal stock that is being priced for the grave. Has the market got it right? Or is it overlooking a whole lotta potential?

The Wizard detects high risk, a hot potato even, but counsels that we must not be deterred from investigating further in case a red hot opportunity really is smouldering deep in the heart of the Rhine Valley…

Cindrigo has a portfolio of renewable energy assets that, on paper, look like a licence to print money. There’s only one small problem. They haven't started any of them.

Its 110MW Combined Heat and Power (CHP) plant in Finland, the Kaipola facility, has been technically ready to go for over a year but has been hamstrung by the collapse of its intended third-party heat offtaker. Meanwhile the company's most valuable asset - three geothermal licences in Germany - remain in the ground, with first power not expected until 2029 and even then after a multi-million euro drilling campaign. This has left the company burning cash, with a market capitalisation of just £18m at a share price of 4.75p (prior to the April 2026 equity raise), implying the market doubts it will succeed.

So far we see a picture of a classic jam tomorrow blue sky venture.

But against this, we must consider the exigencies of the European energy transition. Wind and solar are intermittent and the grid buckling under the strain. Germany desperately needs baseload, low-carbon energy to replace Russian gas and its Energiewende - or long-term energy strategy - provides powerful tailwinds for companies like Cindrigo. The Government is absolutely rooting for Cindrigo to succeed, ‘walking the talk’ as CEO Lars Gulstrand says, throwing huge financial incentives at the company. Consider also that as a source of energy, Geothermal is the weapon of choice right now, matching nuclear for reliability and capacity (at over 90%+) without the risks nuclear poses.

Add to that geothermal is already being widely used in Germany with very generous offtake prices and financing arrangements set in law. On paper (how easy that is to say) Cindrigo’s geothermal assets will be absolute cash-gushers if management can fire them up.

So we see two simultaneous narratives: one of despondency and even despair, the other of hope and promise. Which of the two is it?

Let’s unpack Cindrigo Holdings’ holdings.

The Opportunity

Cindrigo’s portfolio has two business units:

Finland – The Biomass Plant (Kaipola)

Cindrigo owns 90% of a 110 MW biomass Combined Heat and Power (CHP) plant in Kaipola. The plant is built and in the ramp-up phase.

This plant burns wood-based fuel to produce both electricity and heat at the same time. The electricity goes to the grid, while the heat can be sold to nearby factories, district heating systems, or other industrial users. The plant itself is already built, but it’s not yet running at full capacity — it’s still in the ramp-up/commissioning phase.

What makes this more interesting than a standard biomass plant is the Fuelwood Finland JV. Cindrigo currently owns 20% of Fuelwood, but it has the right to increase that stake to a majority over time. The idea here is that Fuelwood will act as a built-in buyer for the heat the plant produces (a ‘captive offtaker’), while also throwing off management fees to Cindrigo. In simple terms: they’re trying to secure demand for the heat on one side while keeping the option to own more of the offtaker on the other.

It’s a reasonably smart structure - it de-risks the plant’s revenue while giving Cindrigo meaningful upside through increased ownership in Fuelwood.

Germany – The Geothermal Play

This is where most of the excitement (and risk) sits. Cindrigo owns 85% of Zukunft Geoenergie GmbH (ZGG), which holds three geothermal exploration licences in Germany’s Upper Rhine Valley — Eich (the main one), plus Worms and Weinheim.

Last week, the company released a new subsurface study on the Eich licence. To say the results are impressive is an understatement: they increased the estimated exploitable geothermal potential to 157.8 MW - a 50% uplift from previous numbers. On top of that, they’re also seeing meaningful lithium in the brine, with a potential output of around 7,230 tonnes per year of lithium carbonate equivalent.

But we must note this is still early-stage. The first well (EichGT-1) is targeted for drilling in 2027, with first power not expected until 2029. So while the resource numbers got better, this is still very much a pre-drilling geothermal story. The lithium angle is a nice potential kicker, but it’s secondary to proving the project can actually produce power.

In spite of this, is there any cause for excitement?

The Financials: A Cash Gusher in Waiting

The German government is absolutely desperate to get Cindrigo’s projects online. Under the German EEG 2023 legislation, geothermal operators receive a statutory Feed-in Tariff (FiT) of €252/MWh - fixed for 20 years. This is a sovereign-backed annuity which, at €252/MWh, means Cindrigo will be operating at an 88% gross cash margin assuming they can get their operations online.

There are taxes to consider and they are not low, but even after the state takes its cut the post-tax cash conversion is still a staggering 61.7%.

Now let’s look at revenues and FCFEs. Are you sitting comfortably?

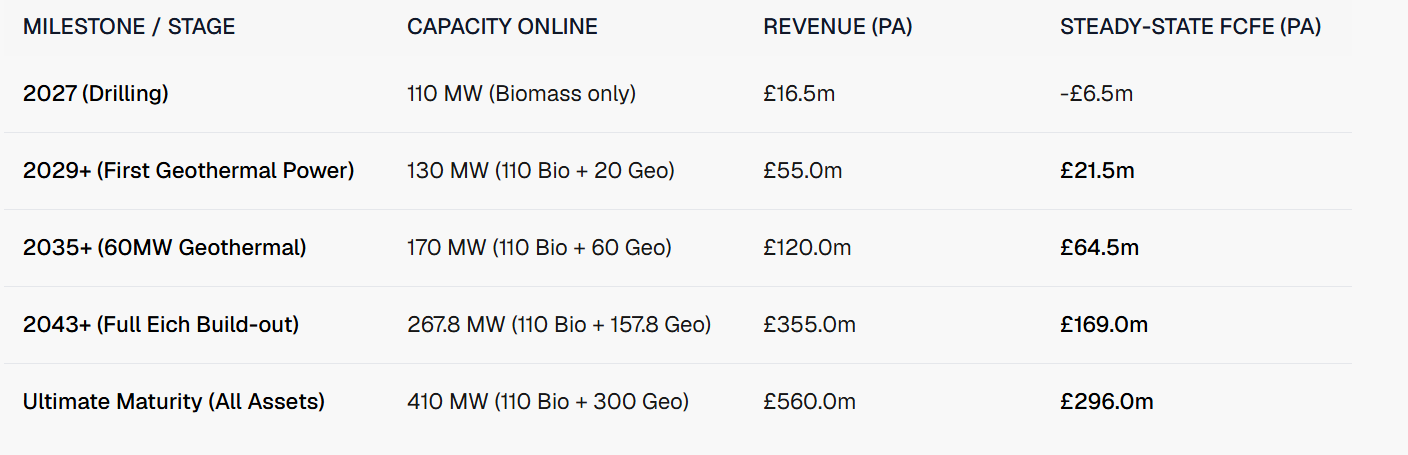

Looking at the key milestones, this is the sheer scale of the opportunity on offer:

All going to plan, by 2029 Cindrigo will be printing more than its entire current MCAP in FCFEs alone.

What this means is that if management just completes Phase One - or a mere 12.6% of the total Eich resource - Cindrigo will generate £21.5m of FCFE per year. Now took at the FCFEs in the table assuming all assets come online. In the scenario Cindrigo is a multi-billion pound company. And the lithium is in for next to nothing.

That’s not a 10x. On these numbers it’s closer to a 100x. The market is pricing in a funeral; the financials suggest a fireworks display. (Readers might note at this point that completing the DCFs for Cindrigo to any degree of accuracy was really really difficult). There’s a lot more I can share here, but one for another post, and let’s move on to the risks.

The Risks, their mitigation - and the odds of success

Now for some rock hard reality checks. In pricing Cindrigo at a lowly £16m, the market hasn’t completely lost its marbles. So before we crack open the Gewurztraminer at the £296m FCFE endgame, let’s look at what if anything might send CINH to zero. Let’s also consider how these risks might be mitigated and estimate the chances of each happening.

1. Induced Seismicity (The Literal Earthquake Risk)

This is the elephant in the Upper Rhine Valley. Geothermal projects inject water at high pressure to fracture hot rock. In a tectonic rift valley like the Rhineland this can cause earthquakes. In 2019, a project in Vendenheim triggered a 3.6 magnitude quake, damaging homes. Germany now enforces a strict ‘Traffic Light System. Hit the red threshold, and the regulator permanently revokes the operators’ licence. Game over.

Mitigation: Cindrigo must use advanced 3D seismic to avoid known fault lines and strictly adhere to the Traffic Light System’s flow-rate adjustments. Crucially, they have secured Munich Re drilling insurance, which covers up to 90% of drilling capital if a red-light seismic shutdown occurs. The licence might die, but the equity at company level receives significant protection.

Probability of Success: 85%

2. Dry Hole Risk

Until the drill bit hits 160°C brine at 3,000 metres, investors are gambling. If the flow rates aren’t high enough, or the temperature is lower than modelled, the economics of that €252/MWh FiT collapse. The company can’t claim a sovereign annuity if it can’t produce the heat.

Mitigation: Eich is not a wildcat; it sits in the heavily proven Upper Rhine Valley rift system where regional well data derisks the subsurface model. Furthermore, the Munich Re insurance also covers dry holes, reimbursing 90% of the drilling capex.

Probability of Success: 80% - still needs the drill bit to hit the brine.

3. Capex Risk & The Funding Gap (Who Pays for the Drilling?)

Deep drilling is ruinously expensive. A single well doublet at Eich costs €30-35m. If Cindrigo had to fund this itself, it would mean a massively dilutive equity raise at a sub-5p share price, wiping out the upside. Capex overruns are also notorious in deep geothermal - stuck drill pipes or stimulation failures can blow the budget by 20% in months.

Mitigation: This is where the German government’s desperation becomes Cindrigo’s shield. The capex structure for Eich is radically different to a standard junior miner:

BEW Module 2 Grant (Government): Covers 40% of eligible drilling and surface capex.

KfW Project Finance (State Bank): Covers roughly 40% of the remaining costs via non-recourse, low-interest debt.

Cindrigo Equity: The equity cheque is reduced to just 10-15% of total capex.

Because the April 2026 equity raise (£6.7m) was done at a premium (12p) (well played management!), Cindrigo has the cash on the balance sheet right now to fund its portion without diluting current shareholders. If capex overruns hit, the BEW grant absorbs 40% of the overrun, and KfW buffers another 40%. The equity exposure to cost blow-ups is mathematically capped. Management must still secure the BEW grant approval and finalize KfW terms prior to spudding.

Probability of Success: 70% (Overruns are likely, but the grant/debt structure absorbs the majority of the pain).

4. Grid Connection (The Bureaucratic Bottleneck)

A 20-year statutory FiT at €252/MWh is a beautiful thing. It is also entirely useless if you cannot plug your plant into the grid. Germany’s grid operators are drowning in renewable connection requests. Securing the Konformitätsbescheinigung (conformity certificate) and physical substation upgrades can delay projects by 2-3 years.

Mitigation: Management must secure the grid connection certificate before Final Investment Decision (FID). No grid cert = No KfW loan = No drilling. It is a binary prerequisite that must be locked down in 2026/2027.

Probability of Success: 75%

5. Project Finance Covenants (The Cash Sweep Trap)

KfW provides non-recourse debt, meaning if the project fails, the bank takes the keys, not Cindrigo’s other assets. But this debt comes with strict Debt Service Coverage Ratios (DSCR). If the plant underperforms during its 12-month ramp-up, a DSCR breach triggers a ‘cash sweep’ - 100% of cash flow is diverted to pay down the bank debt, and Cindrigo HoldCo gets zero dividends.

Mitigation: Management must model conservative Initial Production (IP) rates and fund a 6-month Debt Service Reserve Account (DSRA) upfront from the equity cheque to buffer any early ramp-up shortfalls.

Probability of Success: 80%

6. Kapiola Execution

The Finnish biomass plant has a track record of missing targets due to third-party off-taker failures. Further delays will accelerate the corporate cash burn and undermine management credibility.

Mitigation: The Fuelwood JV structurally fixes the off-taker problem by internalizing the heat demand, and throws off €75k/month in management fees. Management must execute the Kaipola ramp-up in late 2026 to halt corporate cash burn and prove operational competence.

Probability of Success: 75%

The Wizard’s Verdict on Risk

When you stack these probabilities up, the path to total loss (the -100% downside) requires a catastrophic, uninsured geological failure or a seismic revocation. The Munich Re insurance and the state grants fundamentally alter the risk profile. You are not risking 100p to make 100p. You are risking a heavily insured downside for a 10.3x base-case upside.

That is why the probabilistic risk/reward asymmetry is 17.2 : 1. The market is pricing the drill risk as if Cindrigo is an uninsured wildcatter. It is not. It is a state-subsidised, insured appraiser holding a 20-year sovereign contract. Remember, failure to operationalise the assets are in no-one’s interests and the Government is desperate for high baseload geothermal projects to succeed. Cindrigo is in the box seat here but yes, it must still deliver.

We also need to discriminate between an above-the-waterline risk, and a below-the-waterline risk - I have written more on this below.

Is management up to the job?

When you’re betting on a company trying to pull off a half-billion-pound energy infrastructure play from a penny-stock position, management isn’t just important - it’s pretty much the whole ballgame. You need people who have been in the trenches, know where the landmines are, and have the sheer willpower to drag a project across the finish line.

Cindrigo has assembled a team that, on paper at least, ticks every single one of those boxes. These are heavy hitters with deep sector scars and serious skin in the game. Let’s break the ‘Fab Four’ down:

First up, Lars Guldstrand (CEO). With 35 years of energy executive experience, Lars has been around the block long enough to know what a baseload power cycle looks like. He owns over 5% of the company, so his fortune is tied directly to those of the shareholders. Yes, he missed the original Kaipola 2025 start target - a clear failure. But Lars also played a blinder by engineering the Fuelwood JV to fix the off-taker mess and raising £6.7m in April 2026 at 12p - a staggering 150% premium to the 4.75p market price was pure genius. You don’t convince institutions to pay a 150% premium in a hostile market by some good ole boy spiel; this needs deep institutional trust. (Note that Danir AB, the Swedish specialist green energy company owns 27.5% of CNH)

Then there’s the Chairman, Jörgen Andersson. He’s the political fixer, a former Swedish Energy Minister. When you are trying to build deep geothermal in Germany, you aren’t just dealing with physics; you are dealing with politics. Andersson waded into the morass of German bureaucracy and walked out with BEW Module 1 extensions for all three licences. You don’t get German state aid without heavy political lifting, and having a former Energy Minister opening doors at BAFA and KfW is an absolute tactical advantage. We’re expecting more of the same with the Conformity Certificates (see 4 in risks above).

Holding the purse strings is Dag Andresen (CFO), a former CFO of Vattenfall. That matters. He knows how big European utilities finance and run multi-million-euro energy projects. He brought proficient supervision to the balance sheet taking a pile of toxic, dilutive convertible notes that were suffocating the company and restructuring them into clean equity. Our kind of magician. Better yet, his capital allocation strategy is refreshingly ruthless: leverage non-dilutive German state aid instead of endlessly printing shares. A CFO who actually hates dilution? We love to see it.

And finally, the guy actually reading the rock: Ishtiaq Ahmad, the Technical Lead and ex-MOL Group E&P Director. He brings the subsurface credibility that transforms this from a promo story into a drillable prospect. It was Ishtiaq who oversaw the recent 50% resource upgrade at Eich. When a guy with his exploration pedigree says the exploitable potential just jumped to 157.8 MW, that does engender respect.

The Verdict: Since April 2026, this team has proved they can raise premium cash, clean up the balance sheet, and play the German bureaucratic game better than most. They’ve navigated the funding and the politics. Now comes the only test that matters - execution on the drill bit. That’s the final exam, and it’s coming up fast.

Valuations mein Schatz

So let’s put it all together and see first how Cindrigo stacks up first against other major geothermal operators, then via cashflows in our own DCFs.

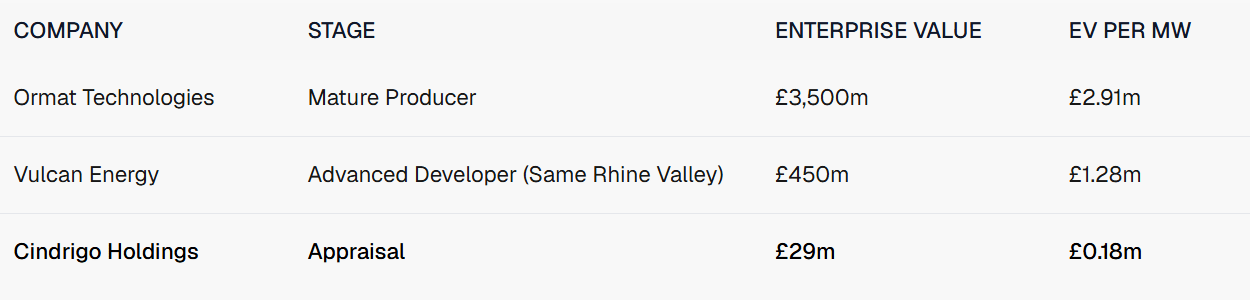

First the players:

When you look at the EV/MW multiples, the disconnect is staggering. Vulcan Energy, sitting in the exact same Upper Rhine Valley with the same geothermal/lithium narrative, is valued by the market at £1.28m per Megawatt. Ormat, the mature global producer, commands £2.91m per Megawatt.

Cindrigo? It’s changing hands at a mere £0.18m per Megawatt.

That is an 85% discount to its closest peer, and a 95% discount to a mature producer. The market is telling us it doesn’t think Cindrigo will pull the iron out of the fire.

Let’s analyse these risks again, stack them together, assume zero value for management (neither positive nor negative) and apply Bayesian adjustments focusing only on ‘below the waterline’ threats (ie existential and not delay), and we arrive at a probability of success of 65%.

That leaves a 35% probability of a total, below-the-waterline failure.

Now, let’s do the maths in away that markets can’t (or don’t).

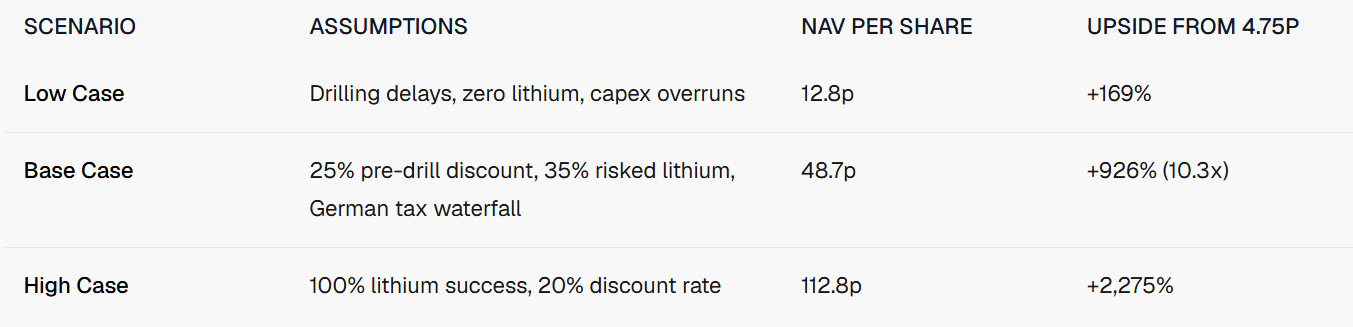

If Cindrigo succeeds (65% probability), using our stringent DCF methodology - using zero terminal value, a 25-year explicit forecast, and the brutal German tax waterfall - gives us a Base Case NAV of 48.7p. That is a gain of 43.95p per share from today’s 4.75p price.

If we assume Cindrigo fails (35% probability), the standard market view is that the equity is effectively zero. Shareholders lose 4.75p per share. Auf Wiedersehen Pet.

But hold on. A below-the-waterline failure in Germany does not mean the equity goes to zero. Why? Because of Finland.

Remember Kaipola? The boring, prosaic biomass plant that the market currently hates? In our Sum-of-the-Parts (SOTP) DCF, the standalone value of the Kaipola/Fuelwood biomass segment is calculated at a base case of £45m, or roughly 11.5p per share.

If the geothermal project suffers a catastrophic failure, Cindrigo falls back to being a slow-growth Finnish biomass company. The stock might drift back down to its intrinsic biomass floor of 11.5p (or perhaps a discounted 8p-9p). But shares can be picked up today at 4.75p.

So, even in the 35% failure scenario, the downside is effectively capped by a hard asset that is worth double the current share price. There is a safety net made of Finnish wood pellets.

Let’s recalculate the asymmetry with this Finland Floor in mind:

Upside (Geothermal Success - 65% probability): The stock goes to 48.7p. Shareholders make 43.95p per share.

Downside (Geothermal Failure - 35% probability): The stock falls back to its biomass floor of 11.5p. Shareholders might still see a 6.75p profit per share.

This isn’t just asymmetric; it’s absurd. Heads, shareholders win a 10x multi-bagger. Tails, they still double their money on the biomass asset. The market is currently valuing the 157.8 MW German geothermal optionality—backed by a €252/MWh sovereign FiT and Munich Re insurance—at less than zero. The geothermal - Cindrgo’s main draw - is in for free.

Earlier, using a binary win/lose model, we calculated a probability-weighted upside of 28.57p versus a downside of 1.66p (a 17.2 : 1 risk/reward).

But the Finland Floor breaks that model entirely. When the ‘downside’ scenario yields an 11.5p share price—a 6.75p profit per share from today's 4.75p entry - the risk of capital loss approaches zero. You aren't risking £1.66 to win £28.57; you are getting paid to take the 65% chance at a 10x return. That isn't just a favourable trade; it's basically a free hit.

And 48.7p is just the base case. If the lithium DLE technology actually works at scale, and the discount rates compress as the de-risking milestones are hit, the High Case NAV leaps to 112.8p. That’s a 23x upside.

The market is looking at the -£6.5m FCFE cash burn in 2027 and pricing Cindrigo for the grave. It is entirely blind to the £21.5m annual free cash flow gusher that follows in 2029, scaling relentlessly to £169m as the full Eich resource is unlocked. This is why we need to model cashflows using a DCF - it dispels short-termism and is a bit like a crystal ball, looking into the future.

The Verdict

Cindrigo is a binary bet, yes. It is a hot potato. But it is a hot potato where the downside is heavily insured and the upside backed by a 20-year German government contract on highly favourable terms.

CINH itself is a long slow burn to full value but where we stand now the market is pricing the drill risk as if Cindrigo is an uninsured wildcatter, and that it is not. It is a state-subsidised, insured appraiser sitting on a smouldering resource beneath the Rhine. If management successfully spuds EichGT-1 in 2027, the market will have no choice but to start closing that 85% valuation gap to its peers.

High risk? Absolutely. High reward? Seismic. The Wizard? Well, let’s just say he’s weighed in with a spud stake.

Looks very promising as its price chart is also beginning to look pretty good. I already have a small stake in it and will add more when its uptrend is in motion.

I have separated out the numbers for Kaipola as a standalone and posted on my Substack Notes section Wizards - not looking bad at all!