Audioboom (and Wizard) deliver...

Today’s stellar results, Wizard’s uncanny crystal ball, and why Fair Value just ticked up to £22.85.

Audioboom Group PLC #BOOM.L BOOM 0.00%↑ .L 495p / £89.7m

Upside: 5x

Dear Wizards,

Well the numbers certainly did the talking today didn’t they?

This morning, Audioboom ($BOOM) dropped its H1 2026 results and with them vindicated Wizard’s unconstrained model in support of the company’s £22.50 valuation made yesterday. Today’s results were so stellar in fact that we are further adjusting our target price higher a notch to reflect Audioboom’s accelerated cash flow in our FCF model.

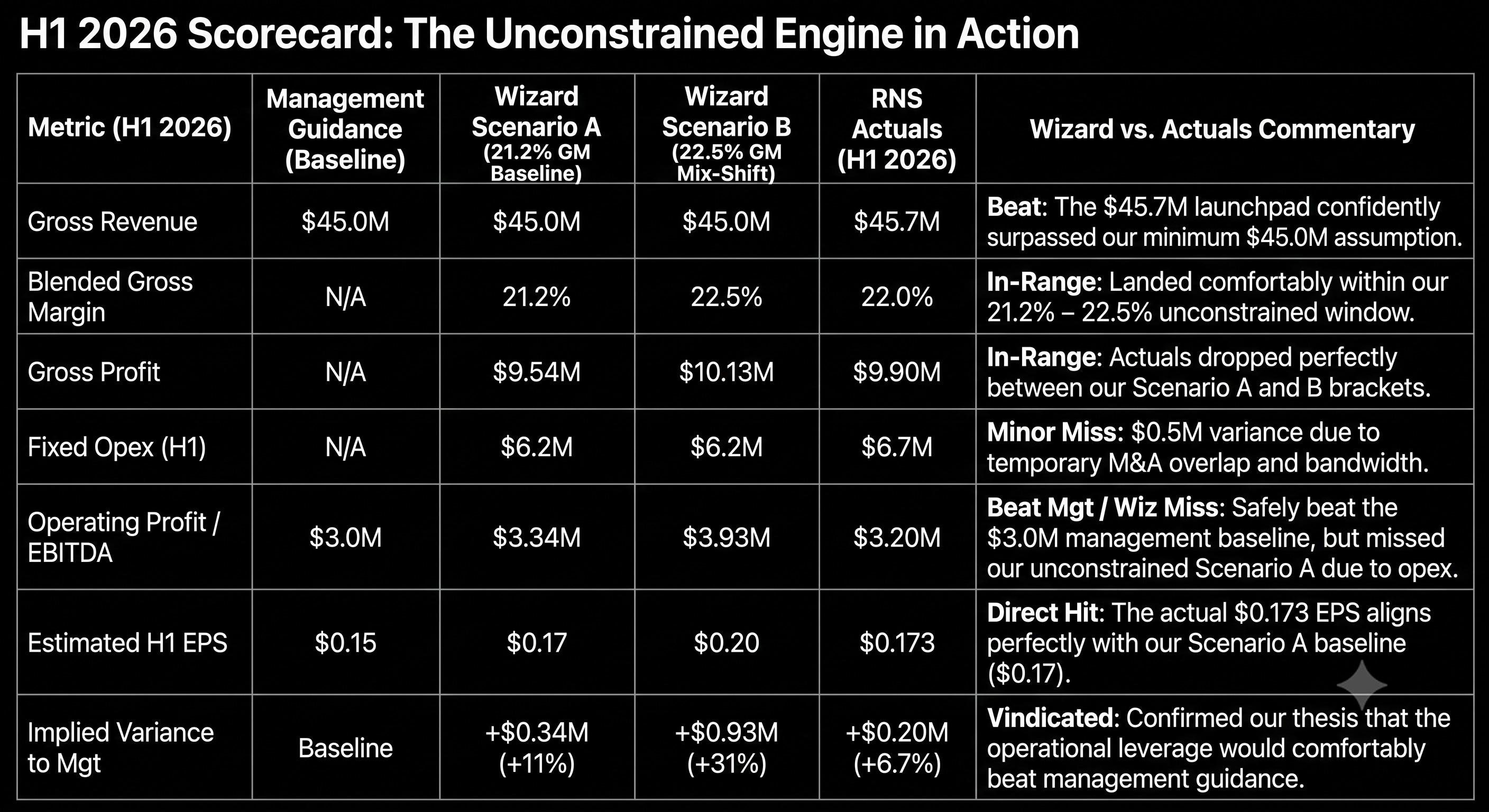

Wizard’s uncanny accuracy

Yesterday evening I stuck my neck out and posted Wizard’s predictions for today’s H1 numbers on X in advance. I did this because I have total confidence in Wizard’s predictive accuracy.

Today’s results have been added to the table and you can be the judge on the accuracy.

Overall Wiz nailed the Operational leverage thesis shared in yesterday’s post and which CEO Stuart Last referred to in today’s presentation. Gross Margins and Gross Profit came bang in the middle of Wiz’s range, Opex admittedly being slightly higher. When it came to the all-important EPS Wiz scored a direct hit, correctly recognising this would come in ahead of Management’s already raised guidance.

This outcome validates Wizard’s forensic, bottom-up methodology. By building our models on causal priors - specifically the interplay between LTV, NRR, margins, and revenue - we can confidently chart a business's true trajectory. Bear in mind Wiz lacks the information Management and Brokers are privy to, gaining insight instead solely by reverse-engineering the business into its core causal drivers.

Applying this directly to Audioboom, our thesis of an ever-increasing Free Cash Flow flywheel has been borne out. The operational leverage we detailed yesterday, which drove our £22.50 valuation, was on full display in today's RNS. The good news for shareholders is that the core narrative is confirmed: Audioboom is going Va-Va-Voom.

Let’s open the bonnet on today’s RNS to see what Management had to say and what that means for shareholders.

The H1 2026 Scorecard: BOOM’s Unconstrained Engine in Action

The H1 numbers show that the ‘pros and cons’ debate is over; the RNS confirmed that the structural profitability of Audioboom’s platform has crossed the tipping point and that it is unequivocally a cashflow machine.

The top hits from today’s Results confirm that:

Massive top & bottom line Beat: Revenue hit US$45.7 million (up 30% YoY), comfortably beating the minimum guidance. More importantly, Adjusted EBITDA surged 80% to US$3.2 million. A 30% increase in revenue driving an 80% increase in profit is the textbook definition of the operational torque we outlined yesterday.

The US midterm catalyst (the big H2 tailwind): CEO Stuart Last commented that Audioboom has achieved over 500 million monthly advertising impressions in the political and news verticals (via partners like Crooked Media and Associated Press).

We are heading into the 2026 US Midterm Elections where political ad spending is price-insensitive and where campaigns buy inventory on a ‘must-win, whatever-it-costs’ basis. This influx of capital will cause RPMs (pricing) to spike across Q3 and Q4.

Because Audioboom has essentially already covered its fixed opex floor for the year, every extra dollar generated from these premium political RPMs drops down almost entirely as free cash flow. This is a massive further catalyst the market is completely ignoring. Long story short, fasten your seatbelts because there is gonna be another upgrade ahead!

H2 Safety and Visibility: Audioboom has already booked US$81 million in revenue for 2026 as of mid-July. The key point here is that BOOM has already surpassed the entirety of 2025’s total revenue (US$80.4 million) before even entering the seasonally strongest half of the year.

Showcase is now the dominant force: Showcase revenue surged 60% YoY to US$18.6 million. It now accounts for 41% of total group revenue (smashing Wiz’s full-year expectation of 38%). This rapid mix-shift into high-margin automated ad insertion is the primary driver behind the gross margin expansion to 22%. The flywheel is picking up speed.

Strategic Independence & Firepower: With the Strategic Review officially concluded and low-ball offers rejected, the speculative arbitrage float has been cleared. The company’s cash balances jumped to US$5.4 million, and they secured an agreement in principle for a US$10.0 million revolving credit facility with HSBC. Audioboom is now fully funded for accretive, non-dilutive M&A consolidation.

Adelicious and the ‘Boutique Agent’ Countermeasure / Moat: The RNS proved our thesis that Audioboom refuses to overpay for talent. Upon connecting Adelicious to Audioboom’s monetisation engine, revenue on their roster increased by 50% in the immediate three months following the deal. Adelicious already delivered £5.5 million in qualifying 2025 revenue. This was achieved for a total net consideration of just £4.53 million, successfully capping the deferred earn-out at a mere £0.9 million (with zero contingent consideration paid) against a maximum potential liability of £10.0 million.

Adelicious has proven to be an absolute steal. Well done management!

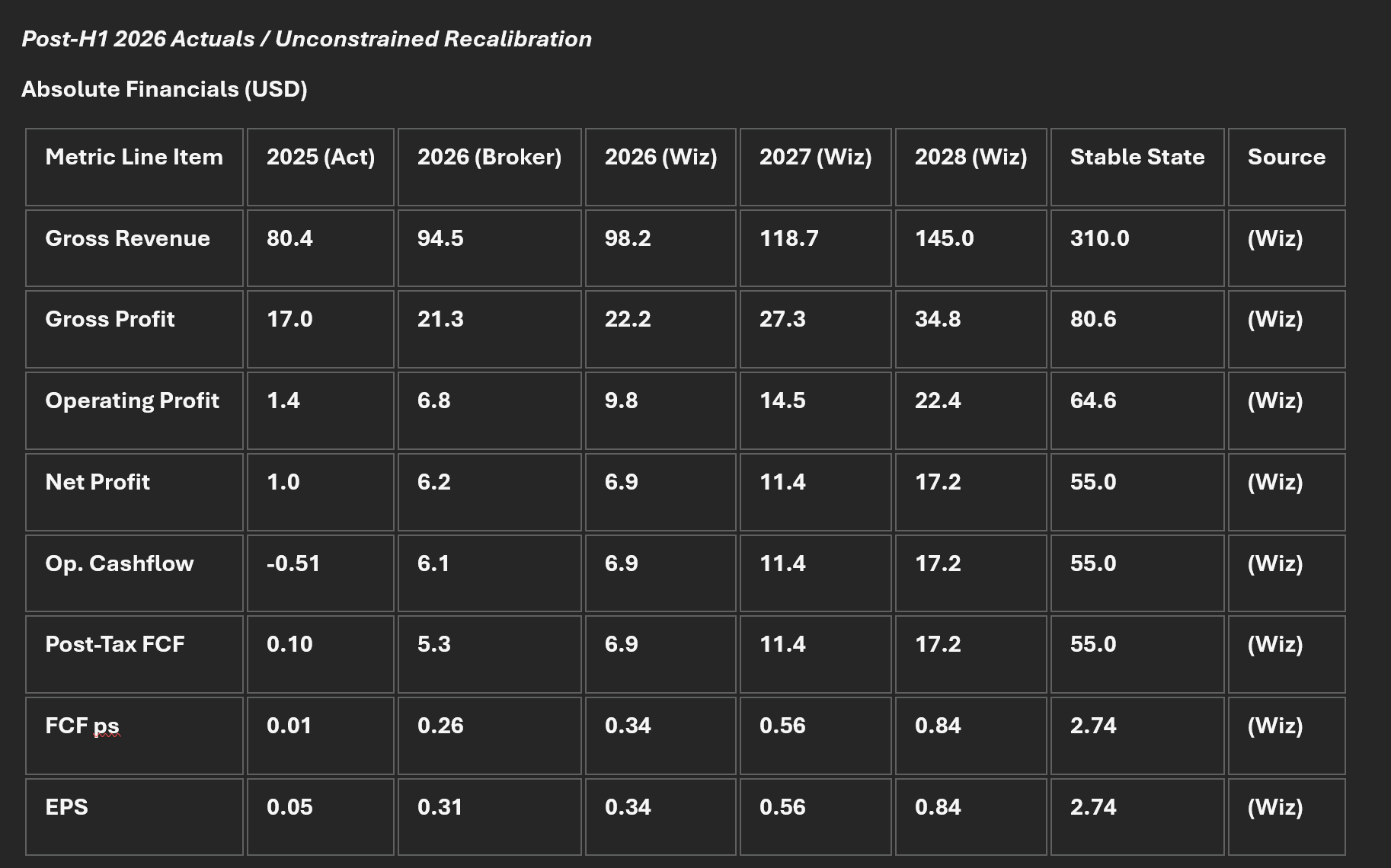

Gear Shift: Revising our numbers up

Today’s blowout numbers force an immediate upgrade to our forward trajectory. H1 revenue of US$45.7 million (+30%) proves our operational leverage model is working faster than forecast, with high-margin Showcase revenue driving overall gross margins to 22%.

The maths here is relatively straightforward: with US$81 million of FY26 revenue already booked, Audioboom already has US$35.3 million in the bag for H2. Once you factor in the new Apple and Spotify video integrations lifting the old yield ceiling, a conservative 15% sequential H2 bump easily carries us to US$52.5 million for the half.

Consequently, Wizard is upgrading our baseline FY 2026 targets:

Gross Revenue: US$98.2 million

Blended Gross Margin: 22.6% (clearing 23.0% in H2)

Operating Profit: US$9.8 million

Free Cash Flow: US$6.9 million

Here are Wiz’s current projections in full:

Thus, at 34 cents, our EPS projection sits well above Cavendish’s current FY26 forecast, and we stand ready to upgrade further based on incoming RNS data.

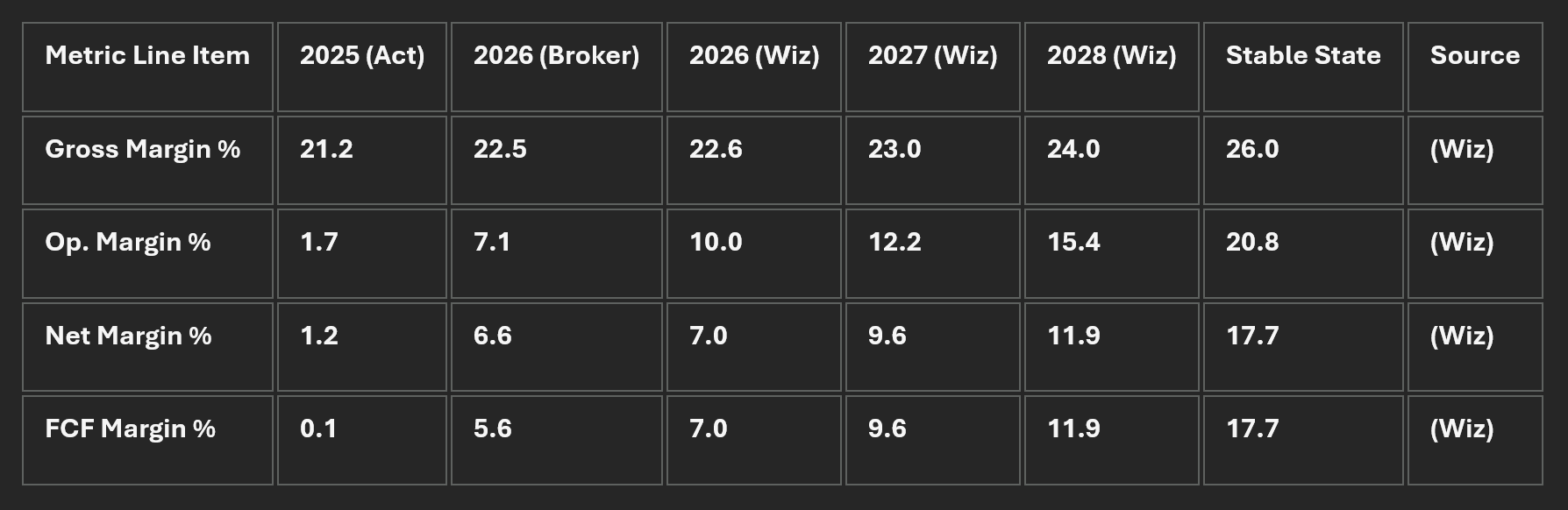

We also see margins expanding:

The Great Broker Disconnect

Despite a record H1 and massive political tailwinds, it is baffling to see Cavendish stubbornly reiterating their 1,300p target price and pessimistic US$94.5 million full-year revenue projection.

Let’s run the numbers. With US$81 million of revenue already booked as of mid-July, Cavendish is effectively telling the market that Audioboom will only generate a measly US$13.5 million in H2 to meet their full-year forecast.

Think about how absurd that is. H2 is seasonally the strongest half of the year for advertising. Yet, Cavendish is forecasting a disastrous second half where the political ad revenues announced by CEO Stuart Last in today’s Results fail to materialise. They are predicting a cataclysmic drop in momentum - modelling a collapse from the 30% YoY growth velocity we just witnessed in H1 down to single digits in H2.

Our position is straightforward: Cavendish is completely out of its depth. It is a matter of major concern for shareholders that Audioboom’s own House Broker cannot grasp the basic platform economics staring them in the face. By failing to understand the simple mathematics of the unconstrained operational leverage we detailed yesterday - which today’s RNS validated - they are actively acting as an artificial drag on the share price.

Their stubborn refusal to upgrade their forecasts in line with the hard data, coupled with their inability to articulate Audioboom’s prodigious cash-generation engine to the broader market, is frankly inexcusable.

They will soon have no choice but to capitulate. Expect a forced, massive upgrade from them around the Q3 update.

En attendant Godot.

Rerate Time

First, a clarification. There have been some raised eyebrows about the valuation given for Audioboom in yesterday’s post.

The confusion may be caused by the House Brokers using a plethora of indicators - including EV/EBITDA, EV/Sales, Sales Growth, EBITDA Growth, and P/E Growth - to determine their version of ‘Fair Value.’ As we saw yesterday, this turns the exercise into a subjective lambada.

As Michael Mauboussin has pointed out, multiples are only indicators of price, not value. They are a heuristic that obscures a company's underlying value drivers, and by themselves, they cannot inform an investor about a business’s true Fair Value.

How do we compute value? Let’s hear it from Warren Buffett:

The value of any stock, bond or business today is determined by the cash inflows and outflows - discounted at an interest rate that makes appropriate allowance for the risk of that investment - that can be expected to occur during the remaining life of the asset.

Warren Buffett

This is precisely the methodology Wizard has followed. By utilising a rigorous Discounted Cash Flow framework - and making Bayesian adjustments to continuously update our priors as new data drops - we model the sum of unencumbered Free Cashflows over the course of the company’s lifetime, discounted by the appropriate interest rate with an additional margin of safety.

For a highly cash-generative machine - which Audioboom is unequivocally proving itself to be - that sum is prodigious. We are right to be amazed. Shareholders have a tiger by the tail here.

The accuracy of Wizard’s modelling has been demonstrated at the top of this post. If our resulting valuation seems outlandish to some, it is not through any flaw in the modelling or the methodology. It is because the House Brokers don’t seem to accept the rigorous valuation standards set by Warren Buffett, Michael Mauboussin, or Aswath Damodaran. Instead, they think sticking a finger in the air at any given moment constitutes a valuation. It does not.

We of course accept that price is dictated by the market. But Fair Value is not—that is determined purely by the discounted sum of a company’s future Free Cash Flows.

Anyway enough of that. Audioboom’s numbers today have led Wiz to bump Fair Value up a notch from yesterday’s £22.50 to today’s £22.85. What a difference a day makes :-)

Today Audioboom delivered in spades, proving that it is an unconstrained cash-flowing juggernaut. I don’t think it will be long for the market to respond in kind.

Va-Va-Voom Wizards.

I have to admit I was more excited reading the RNS than the actual InvestorMeet presentation, which seem to come across rather flat.

Having said that the growth continues at an accelerated pace, while costs stay relatively flat, staff costs were only 44, two more than pre Adelicious acquisition.

The post strategy review story, was made clearer, with $10m HSBC credit being available for four to five acqusitions.

Frustrating that no questions were answered, and address the fundamental issue of the AIM listing was not addressed.

An often overlooked financial asset, is the amount of deferred tax losses that a company can use to minimise tax on profits, thus it can effectively set profits against tax losses for the next few years, and indeed interest from loans also reduce taxable profits.

Annual Report 2025 page 52

The Group has carried forward UK losses amounting to US$36.4 million as of 31 December 2025 (2024: US$39.1 million). The gross amount of losses upon which the deferred tax asset has been recognised amounts to US$8.0 million (2024: US$7.8 million).